Centre Tightens GST E-Way Bill Norms After CAG Flags Systemic Flaws

Government Strengthens E-Way Bill Controls to Plug Compliance Gaps

The Ministry of Finance, in response to observations made by the Comptroller and Auditor General of India (CAG), has confirmed that significant system-level corrections have been implemented in the GST E-Way Bill mechanism.

These reforms aim to curb misuse, prevent tax evasion, and ensure greater transparency in the movement of goods under GST.

The clarification was given in the Rajya Sabha by the Minister of State for Finance, Shri Pankaj Chaudhary, following questions on deficiencies identified by the CAG.

🔍 Background: Why the CAG Raised Concerns

The CAG, during its audit of the GST system, pointed out serious technological and compliance gaps in the e-way bill framework, which could be exploited for:

- Tax evasion

- Fake movement of goods

- Circular trading

- Generation of bogus invoices

The findings highlighted that the system, in its earlier form, lacked robust validation controls.

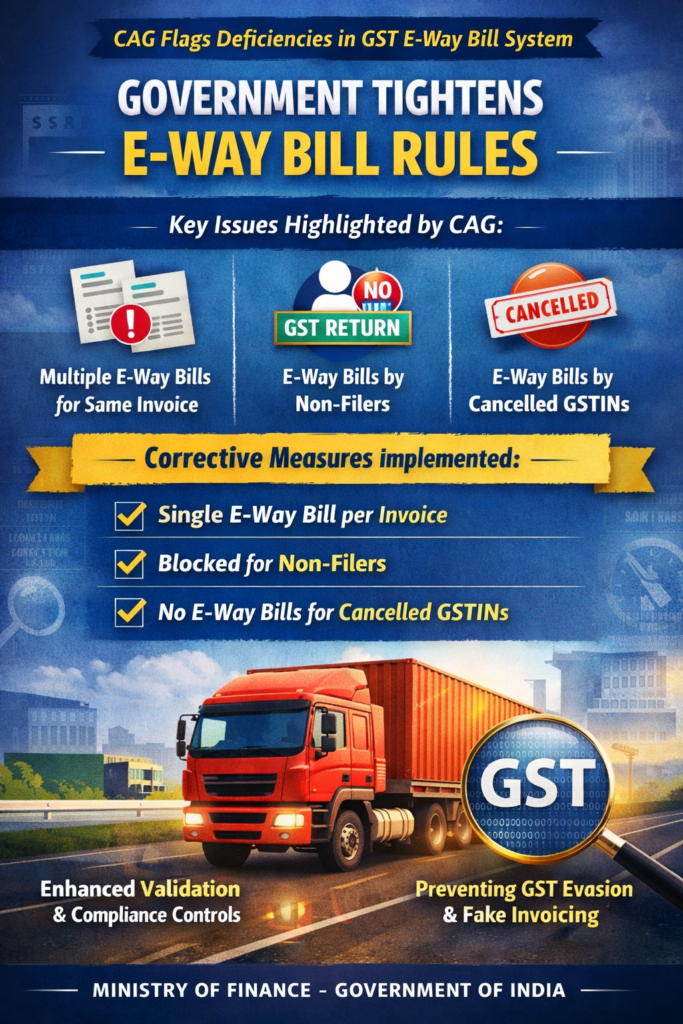

⚠️ Key Deficiencies Identified by CAG

The CAG flagged three major loopholes in the GST e-way bill system:

1️⃣ Generation of Multiple E-Way Bills for the Same Invoice

- Same invoice number used multiple times

- Minor differences in uppercase and lowercase characters allowed duplication

- Enabled repeated movement of goods on a single invoice

2️⃣ E-Way Bills Generated by Non-Filers

- Taxpayers who had not filed GST returns were still able to generate e-way bills

- Increased risk of fake or unaccounted transactions

3️⃣ E-Way Bills Generated Using Cancelled GSTINs

- Even after cancellation of GST registration, some users could generate e-way bills

- Allowed movement of goods under invalid registrations

✅ Corrective Measures Taken by the Government

The Finance Ministry confirmed that system-level validations have now been strengthened to eliminate these loopholes.

✔️ 1. Restriction on Multiple E-Way Bills for Same Invoice

The following controls have now been implemented:

- ✔ Case-sensitive validation introduced

- ✔ Same invoice number + date cannot be reused

- ✔ System rejects duplicate entries

- ✔ E-way bills not allowed for documents older than 180 days

📌 Impact:

Prevents recycling of invoices and misuse for fake transport or tax evasion.

✔️ 2. Blocking of E-Way Bills for Non-Filers

The system now checks:

- Whether the taxpayer has filed last 3 GST returns

- If returns are pending → E-way bill generation is blocked

📌 Impact:

Ensures compliance discipline and forces timely return filing.

✔️ 3. Complete Block for Cancelled GSTINs

- System auto-verifies GSTIN status

- If registration is cancelled, e-way bill generation is completely disabled

- No manual override allowed

📌 Impact:

Prevents movement of goods under fake or inactive registrations.

📜 Official Statement – Ministry of Finance

The Government clarified in the Rajya Sabha:

“The system has been strengthened to prevent generation of multiple e-way bills for the same invoice, restrict non-filers from generating e-way bills, and block cancelled GSTINs from any e-way bill activity.”

This confirms that most of the CAG’s audit observations have already been addressed through technology-driven controls.

⚖️ Legal & Compliance Significance

These changes have major implications for:

✔ GST-registered businesses

✔ Transporters

✔ Accountants & tax consultants

✔ GST audit and litigation cases

Key Takeaways:

- No scope for duplicate e-way bills

- Return filing discipline strictly enforced

- Reduced scope for fake invoicing

- Stronger audit trail for GST authorities

📊 Impact on Businesses & Taxpayers

| Area | Impact |

|---|---|

| Compliance | Increased discipline |

| Litigation | Reduced disputes |

| Tax Evasion | Strongly curbed |

| System Integrity | Significantly improved |

| Audit Risk | Higher detection capability |

🧾 Conclusion

The Government’s response to the CAG findings reflects a clear intent to strengthen GST compliance through technology rather than manual enforcement.

By:

- Eliminating duplicate e-way bills

- Blocking non-filers

- Disabling cancelled GSTINs

the GST ecosystem is moving toward greater transparency, accountability, and real-time control.

These reforms will significantly reduce tax leakage and enhance trust in the GST framework.

GSTN to Block GSTR-3B Filing for Excess ITC Reclaim & Excess RCM ITC: New Validations in Reclaim Ledger and RCM Ledger

GSTN has been steadily moving GST compliance from “warning-based” checks to “hard validations” (system blocks). A key change announced is that negative balances / excess ITC availment beyond available ledger balance will soon not be allowed, and GSTR-3B filing may be blocked until the mismatch is corrected.

This update is especially important for businesses that frequently deal with:

- temporary ITC reversals and later reclaim (e.g., Rule 37/42/43 situations, vendor compliance, disputes), and

- Reverse Charge Mechanism (RCM) payments and ITC claims.

1) What is the “Electronic Credit Reversal & Re-claimed Statement” (Reclaim Ledger)?

GSTN introduced the Electronic Credit Reversal and Re-claimed Statement to ensure correct reporting of:

- ITC temporarily reversed in GSTR-3B Table 4(B)(2), and

- the subsequent reclaim in Table 4(D)(1) and linkage with Table 4(A)(5).

Applicability timeline

- Monthly filers: from August 2023 return period

- Quarterly filers: from July–September 2023 quarter

Where to view (GST Portal path)

Dashboard → Services → Ledger → Electronic Credit Reversal and Re-claimed

2) What is the “RCM Liability/ITC Statement” (RCM Ledger)?

To improve accuracy in RCM reporting, GSTN introduced a separate statement that tracks:

- RCM liability paid in GSTR-3B Table 3.1(d), and

- corresponding ITC claimed in Table 4(A)(2) and Table 4(A)(3) (period-wise).

Applicability timeline

- Monthly filers: from August 2024

- Quarterly filers: from July–September 2024 quarter

Where to view (GST Portal path)

Services → Ledger → RCM Liability/ITC Statement

3) What was happening earlier: “Warning comes, but filing allowed”

Reclaim Ledger (ITC reclaim)

If a taxpayer tried to reclaim more ITC in Table 4(D)(1) than available in the Reclaim Ledger balance, the portal generally showed a warning, but the taxpayer could still file GSTR-3B.

RCM Ledger (RCM ITC)

Similarly, if ITC claimed in Table 4(A)(2)/(3) exceeded the permissible level based on RCM ledger + current Table 3.1(d) liability, a warning appeared.

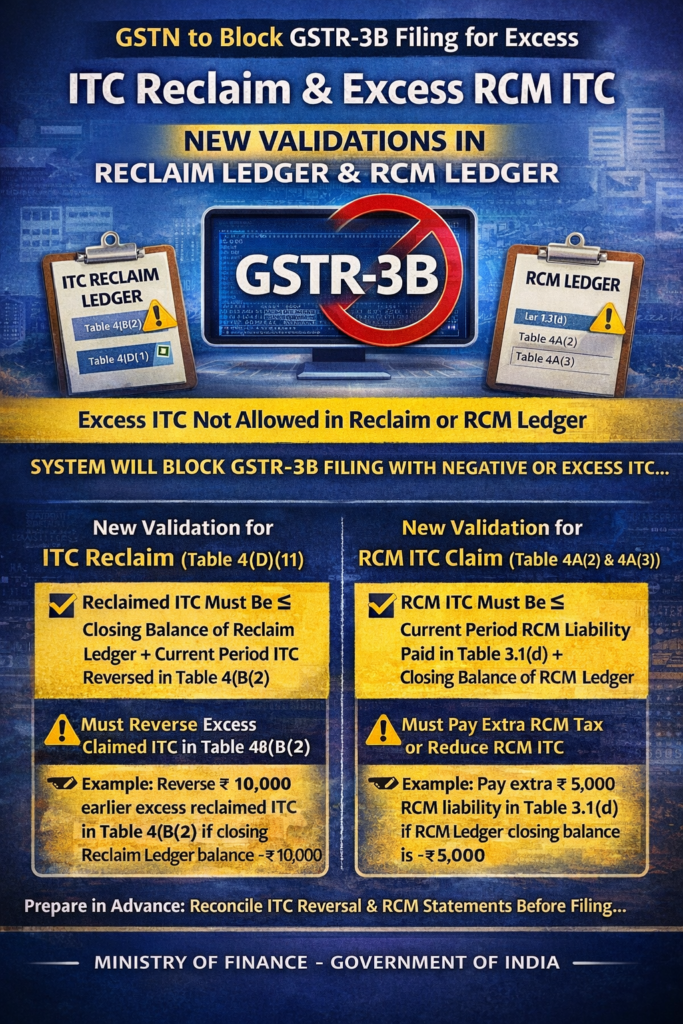

4) What is changing now: “Hard validation” (system will stop excess ITC)

GSTN has informed that shortly the portal will not allow negative values or excess ITC availment beyond available balance in both ledgers.

A) New validation for ITC reclaim (Table 4(D)(1))

Table 4(D)(1) reclaim must be ≤

Closing balance of Reclaim Ledger + current period ITC reversed in Table 4(B)(2)

Meaning (simple):

You can reclaim only what is available in your “reclaim bucket” (ledger), plus whatever you are reversing this period that becomes reclaimable later, as per the portal logic.

B) New validation for RCM ITC claim (Table 4(A)(2) & 4(A)(3))

RCM ITC in Table 4(A)(2)/(3) must be ≤

RCM liability paid in Table 3.1(d) for the same return + closing balance of RCM ledger

Meaning (simple):

You cannot claim RCM ITC unless the system sees matching RCM tax paid (current period) or sufficient eligible balance already reflected in the RCM statement.

5) Big impact: If your closing balance is already negative, GSTR-3B may be blocked

GSTN has clearly stated that if a taxpayer already has negative closing balance in either statement, GSTR-3B filing will not be allowed until corrective action is taken.

A) If Reclaim Ledger closing is negative

You must reverse the excess claimed ITC by reporting reversal in Table 4(B)(2) of current period.

If no ITC is available, that reversal may get added to liability while filing.

Example (from advisory logic):

If ledger shows –₹10,000, it means ₹10,000 excess ITC was reclaimed earlier. You must reverse ₹10,000 in Table 4(B)(2) to proceed.

B) If RCM Ledger closing is negative

You must either:

- Pay additional RCM liability in Table 3.1(d) equal to negative balance, OR

- Reduce ITC claim in Table 4(A)(2)/(3) to permitted level.

Example (from advisory logic):

If RCM ledger shows –₹5,000, you must either pay ₹5,000 more RCM in 3.1(d), or reduce RCM ITC claim by ₹5,000.

6) Practical “Do this before filing GSTR-3B” Checklist (for clients)

✅ Step 1: Check both statements

- Reclaim Ledger: Services → Ledger → Electronic Credit Reversal and Re-claimed

- RCM Ledger: Services → Ledger → RCM Liability/ITC Statement

✅ Step 2: Ensure you are not exceeding validations

- Confirm Table 4(D)(1) reclaim is within allowed limit

- Confirm Table 4(A)(2)/(3) RCM ITC is within allowed limit

✅ Step 3: Fix negative balances before filing

- Negative Reclaim Ledger → reverse in 4(B)(2)

- Negative RCM Ledger → pay RCM in 3.1(d) or reduce ITC in 4(A)(2)/(3)

✅ Step 4: Document your working papers

Keep internal working for:

- invoice/vendor wise ITC reversal basis

- RCM liability vs ITC mapping

This will help during departmental queries and audits.

7) Why GSTN is doing this (professional view)

This change is a classic move towards system-driven compliance, because:

- ITC reclaim (4D(1)) is a sensitive area where clerical errors easily happen

- RCM is often mismatched due to payment timing differences and missed claims

- Once hard validations start, incorrect reporting becomes impossible to file, reducing misuse and future disputes.

Conclusion

The message is clear: warnings are evolving into filing restrictions. Taxpayers should immediately reconcile:

- ITC reversals vs reclaim (Table 4B(2) ↔ 4D(1)), and

- RCM tax paid vs ITC claimed (Table 3.1(d) ↔ 4A(2)/(3)),