Paying income tax is a legal responsibility, but paying more tax than required is not. The Income-tax Act provides several deductions, exemptions and planning opportunities that can legally reduce your tax liability. The key lies in understanding these provisions and planning your finances throughout the financial year instead of rushing for tax-saving investments just before filing your Income Tax Return (ITR).

Whether you are a salaried employee, doctor, freelancer, consultant, business owner or senior citizen, proper tax planning can help you:

Reduce your tax liability legally.

Improve cash flow.

Avoid unnecessary tax notices.

Build long-term wealth.

Stay fully compliant with the Income-tax Act.

In this comprehensive guide, we explain practical tax-saving strategies that every taxpayer should understand in 2026.

Who Should Read This Guide?

This article will be useful for:

✔ Salaried Employees

✔ Pensioners & Senior Citizens

✔ Freelancers & Consultants

✔ Doctors, Chartered Accountants & Other Professionals

✔ Small Business Owners

✔ Investors in Shares, Mutual Funds and Property

✔ Anyone looking to reduce tax legally while remaining fully compliant with the law.

Tax Planning vs Tax Avoidance vs Tax Evasion

Many taxpayers use these terms interchangeably. However, they are completely different concepts.

Understanding the difference is essential before planning your taxes.

Particulars

Tax Planning

Tax Avoidance

Tax Evasion

Meaning

Arranging finances within the provisions of the Income-tax Act to reduce tax liability.

Exploiting loopholes or technical gaps in tax laws to reduce tax.

Deliberately concealing income or furnishing false information to evade tax.

Legality

Fully legal and encouraged.

Generally legal but may be challenged if it defeats the intent of the law.

Illegal and punishable under the Income-tax Act.

Objective

Minimise tax through legitimate deductions, exemptions and planning.

Reduce tax by taking advantage of legal technicalities.

Avoid payment of tax by fraudulent means.

Examples

Investing in eligible tax-saving instruments, claiming allowable deductions, choosing the appropriate tax regime.

Artificial business structures or transactions designed solely to reduce tax.

Interest, penalties, prosecution and reputational damage.

Tip: Always remember that the objective is tax optimisation, not tax evasion. A good tax plan reduces taxes legally while keeping you fully compliant with the Income Tax Act.

Legal Tax-Saving Tips at a Glance

Before discussing each strategy in detail, here is a quick summary.

✅ Choose the most beneficial tax regime.

✅ Start tax planning from April—not March.

✅ Claim every eligible deduction and exemption.

✅ Plan capital gains before selling investments.

✅ Report every source of income accurately.

✅ Use presumptive taxation where eligible.

✅ Pay Advance Tax on time.

✅ Download and reconcile AIS and Form 26AS before filing.

✅ Preserve supporting documents.

✅ File and e-verify your Income Tax Return within the prescribed time.

These simple practices can significantly reduce your tax liability while avoiding future compliance issues.

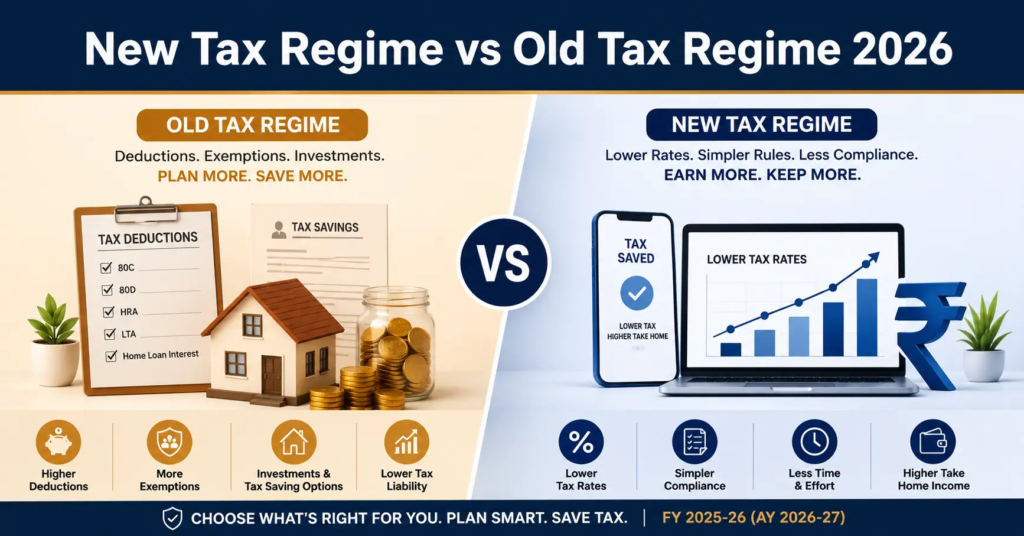

Strategy 1 – Choose the Right Tax Regime

One of the biggest tax-saving decisions is selecting the correct tax regime.

Many taxpayers assume that the New Tax Regime is always beneficial because of its lower tax rates. Others continue with the Old Tax Regime simply because they have invested under Section 80C.

Both assumptions can be costly.

The correct choice depends upon:

Annual income

Eligible deductions

Salary structure

Home loan

Medical insurance

Retirement investments

Other exemptions available

Therefore, calculate your tax under both regimes before making the final decision.

Old Tax Regime vs New Tax Regime

Particulars

Old Tax Regime

New Tax Regime

Default Regime

No

Yes

Tax Rates

Higher

Lower

Standard Deduction

Available

Available (higher limit as applicable)

Section 80C Deduction

Available

Not available (except specified deductions permitted by law)

Section 80D

Available

Not available

HRA & LTA

Available

Not available

Home Loan Interest (Self-Occupied)

Available subject to conditions

Not available

Best Suited For

Taxpayers with significant deductions

Taxpayers with few deductions and a simpler tax profile

Tip: Never choose a tax regime merely because your colleague or friend has selected it. Every taxpayer’s income pattern, deductions and financial goals are different.

Which Tax Regime Should You Choose?

As a broad guideline:

The Old Tax Regime may be beneficial if you:

Claim deductions under Section 80C.

Pay medical insurance premium.

Receive HRA exemption.

Have a self-occupied house with eligible home loan interest.

Make significant retirement investments.

The New Tax Regime may be beneficial if you:

Have limited deductions.

Prefer a simpler tax structure.

Do not wish to make investments solely for tax-saving purposes.

Tip: Tax planning is not about selecting the Old or New Tax Regime. It is about selecting the regime that results in the lowest legal tax liability after considering your overall financial position.

Common Mistake to Avoid

Many taxpayers purchase insurance policies or make last-minute investments merely to save tax without first comparing both tax regimes.

Instead:

Calculate tax under both regimes.

Compare the total tax liability.

Consider your long-term financial goals.

Then make the final choice.

A well-informed decision at the beginning of the financial year can result in substantial tax savings while avoiding unnecessary investments.

Strategy 2 – Claim Every Eligible Deduction and Exemption

One of the simplest ways to reduce your tax liability is to claim every deduction and exemption that you are legally entitled to. Unfortunately, many taxpayers either overlook valuable deductions or invest in products without understanding whether they actually suit their financial goals.

Remember, a deduction should be the result of good financial planning—not the sole reason for making an investment.

Important Deductions Available Under the Old Tax Regime

Deduction

Purpose

Maximum Benefit*

Section 80C

PPF, EPF, ELSS, Life Insurance Premium, NSC, Children’s Tuition Fees, Principal Repayment of Home Loan

₹1,50,000

Section 80CCD(1B)

Additional contribution to National Pension System (NPS)

₹50,000

Section 80D

Medical Insurance Premium

As per the prescribed limits

Section 80G

Eligible Donations

50% or 100% subject to conditions

Section 80TTA

Savings Bank Interest (Non-Senior Citizens)

₹10,000

Section 80TTB

Interest for Senior Citizens

₹50,000

Section 24(b)

Interest on Housing Loan (Self-Occupied House)

Up to ₹2,00,000 subject to conditions

Tip: Never invest in a financial product solely because it offers a tax deduction. First, ask yourself whether it aligns with your financial goals, risk profile and liquidity needs.

Many taxpayers rush to buy insurance policies or make investments during February and March simply to reduce tax.

This often results in:

Buying unsuitable insurance products.

Locking money in low-return investments.

Missing better wealth-creation opportunities.

Poor cash flow management.

Instead, adopt this approach:

✔ Build an emergency fund.

✔ Buy adequate health insurance.

✔ Invest regularly through SIPs.

✔ Plan retirement systematically.

✔ Claim deductions as an additional benefit.

Tax planning should complement wealth creation—not replace it.

Strategy 3 – Plan Capital Gains Carefully

Capital Gains Tax is one of the most misunderstood areas of taxation. With proper planning, however, it is often possible to reduce the tax burden legally.

Before selling any investment, consider:

How long you have held the asset.

Whether the gain will be treated as Short-Term or Long-Term.

Whether you can utilise carried-forward capital losses.

Whether any exemption is available through reinvestment.

Planning before the sale usually provides better tax outcomes than trying to reduce tax afterwards.

Review your gains before the end of the financial year.

Consider tax-loss harvesting where appropriate.

Maintain proper purchase and sale records.

Avoid unnecessary frequent trading merely to save tax.

Real Estate

If you are selling a residential house or another capital asset, evaluate whether you qualify for exemptions available under the Income-tax Act by reinvesting the gains in eligible assets, subject to the prescribed conditions.

Tip: The biggest tax-saving opportunity in capital gains usually arises before you execute the sale—not afterwards.

Strategy 4 – Plan Business and Professional Income Properly

Freelancers, professionals and small business owners have several legitimate tax planning opportunities.

Good tax planning starts with proper record-keeping.

Some practical suggestions:

✔ Keep business and personal bank accounts separate.

✔ Maintain invoices and supporting documents.

✔ Record income regularly instead of reconstructing accounts at year-end.

✔ Choose the appropriate taxation scheme where eligible.

✔ Pay Advance Tax within the prescribed timelines.

✔ Ensure GST compliance wherever applicable.

Proper records not only help in tax planning but also reduce the chances of disputes during assessment.

Small businesses and specified professionals who satisfy the prescribed conditions may opt for presumptive taxation under the Income-tax Act.

This can:

Simplify compliance.

Reduce bookkeeping requirements.

Lower audit-related obligations where applicable.

However, the decision should be made after evaluating the nature of the business, turnover and long-term implications.

Tip: Presumptive taxation simplifies compliance, but it is not automatically the best option for every taxpayer. Review your facts carefully before opting for it.

Strategy 5 – Report Every Source of Income

One of the most common reasons for receiving an Income Tax notice is the omission of small income items.

Today, the Income Tax Department receives information from banks, mutual funds, employers, stock exchanges and various financial institutions. Therefore, it is essential to disclose all taxable income.

Do not forget to report:

Salary

Pension

Savings Bank Interest

Fixed Deposit Interest

Dividend Income

Rental Income

Capital Gains

Freelance or Consultancy Income

Business Income

Income from Side Hustles

Virtual Digital Asset (Crypto) transactions, where applicable

Foreign Assets and Income from Foreign Sources

Always Reconcile with AIS and Form 26AS

Before filing your return:

✔ Download your Annual Information Statement (AIS).

✔ Download Form 26AS.

✔ Match them with your books, bank statements and investment records.

If any discrepancy is noticed, take corrective action before filing the return.

Tip: Never assume that because tax has been deducted at source (TDS), you do not need to report the income. TDS is only a method of tax collection; the income must still be disclosed in your Income Tax Return wherever required.

Dr. B maintains separate bank accounts for professional receipts and personal expenses, preserves invoices, evaluates the appropriate taxation scheme and pays Advance Tax on time.

Result:

Easier compliance.

Reduced chances of notices.

Better cash flow management.

Smooth tax filing every year.

Key Takeaways

✔ Claim every eligible deduction.

✔ Invest according to financial goals—not only for tax savings.

✔ Plan capital gains before selling investments.

✔ Maintain proper business records.

✔ Report every source of income accurately.

✔ Reconcile your return with AIS and Form 26AS before filing.

Strategy 6 – Avoid Last-Minute Tax Planning

One of the biggest mistakes taxpayers make is postponing tax planning until the final few weeks of the financial year. This often leads to hurried investment decisions, poor financial choices and unnecessary stress.

Good tax planning should begin from the first day of the financial year, not in February or March.

Why Early Tax Planning Matters

When you start planning early, you can:

Spread your investments over the entire year.

Improve monthly cash flow.

Avoid unnecessary borrowing.

Select investments based on financial goals rather than tax savings.

Reduce the possibility of missing deductions.

Guru Tip: Tax planning is a year-long process, not a year-end activity.

A Simple Tax Planning Calendar

April – June

Compare the Old and New Tax Regime.

Estimate your annual income.

Start SIPs or other planned investments.

Review your medical insurance.

July – September

Review your tax planning.

Check Form 16 and salary structure.

Verify TDS deductions.

Evaluate home loan benefits.

October – December

Collect investment proofs.

Review deductions.

Estimate Advance Tax liability.

Download AIS and Form 26AS.

January – March

Fill any deduction gaps.

Review capital gains.

Verify all documents.

Prepare for Income Tax Return filing.

Strategy 7 – Maintain Proper Documentation

Many genuine tax deductions are rejected because taxpayers fail to preserve proper supporting documents.

Remember:

A deduction without evidence is simply a claim.

Good documentation protects you during assessments and notices.

Important Documents to Preserve

Salary

✔ Form 16

✔ Salary Slips

✔ Form 12BA (where applicable)

Investments

✔ PPF Statement

✔ ELSS Statement

✔ LIC Premium Receipts

✔ NPS Statement

Medical Insurance

✔ Premium Receipts

✔ Policy Copy

Housing Loan

✔ Interest Certificate

✔ Loan Statement

Capital Gains

✔ Purchase Deed

✔ Sale Deed

✔ Broker Contract Notes

✔ Mutual Fund Statements

Business

✔ Purchase Bills

✔ Sales Invoices

✔ Bank Statements

✔ GST Returns

✔ Books of Account (where applicable)

How Long Should Documents Be Preserved?

As a good professional practice, preserve important tax records for at least 6–8 years, and retain property-related documents even longer wherever they may be required.

Professional Tip: Scan important documents and store them securely in cloud storage. Digital copies are easier to retrieve during tax assessments.

Strategy 8 – File Your Income Tax Return on Time

Filing the return on time offers benefits far beyond avoiding penalties.

Timely filing:

Demonstrates tax compliance.

Facilitates faster refunds.

Helps in obtaining loans and visas.

Preserves the right to carry forward eligible losses, subject to the law.

Reduces the likelihood of notices arising from delayed compliance.

Before Filing Your Return

Always verify:

✅ Form 16

✅ AIS

✅ Form 26AS

✅ Bank Interest

✅ Dividend Income

✅ Capital Gains

✅ Business Income

✅ TDS

✅ Advance Tax

Strategy 9 – Verify Your Return

Many taxpayers believe filing the return completes the process.

It does not.

The return must also be verified (e-verified or otherwise completed in the prescribed manner) within the applicable time limit.

Failure to complete verification may result in the return not being treated as valid.

10 Common Tax Planning Mistakes

Avoid these common errors.

1. Choosing the Wrong Tax Regime

Always compare both regimes before making a decision.

2. Investing Only for Tax Saving

Every investment should support your long-term financial goals.

3. Ignoring Small Income

Savings account interest, FD interest and dividend income must also be reported wherever taxable.

4. Ignoring AIS

Many notices arise due to mismatches between the return and AIS.

5. Waiting Until March

Last-minute tax planning usually results in poor investment decisions.

6. Not Preserving Documents

Without proper evidence, deductions may be questioned.

7. Incorrect Capital Gains Calculation

Capital gains should always be calculated carefully after considering the applicable provisions.

8. Missing Advance Tax

Where Advance Tax provisions apply, delayed payment may result in interest.

9. Not Verifying the Return

Filing alone is not sufficient.

10. Believing Social Media Tax Myths

Always verify information from official sources or qualified professionals.

Tax Planning Checklist Before Filing ITR

Before clicking Submit, ask yourself:

☐ Have I compared both tax regimes?

☐ Have I reported every source of income?

☐ Have I checked AIS?

☐ Have I downloaded Form 26AS?

☐ Have I verified TDS?

☐ Have I claimed all eligible deductions?

☐ Have I checked capital gains?

☐ Have I verified bank interest?

☐ Have I calculated Advance Tax correctly?

☐ Have I preserved all supporting documents?

☐ Have I completed e-verification?

Key Takeaways

Remember these simple principles:

✔ Start planning early.

✔ Choose the correct tax regime.

✔ Claim only genuine deductions.

✔ Maintain proper records.

✔ Report every income.

✔ Verify your return carefully.

✔ Stay compliant with tax laws.

Good tax planning is not about avoiding tax—it is about using the law wisely.

Conclusion

Reducing your tax liability legally is not about discovering secret loopholes or making last-minute investments. It is about understanding the Income-tax Act, making informed financial decisions and planning throughout the financial year.

Whether you are a salaried employee, freelancer, professional, business owner or senior citizen, disciplined tax planning can help you optimise your tax liability while remaining fully compliant with the law.

Most importantly, remember that tax-saving should never become the sole objective of financial planning. Investments should first help you build long-term wealth, achieve financial security and meet life goals. The tax benefit should be viewed as an additional advantage—not the primary reason for investing.

By choosing the appropriate tax regime, claiming eligible deductions, reporting every source of income accurately, maintaining proper documentation and filing your Income Tax Return on time, you can minimise your tax burden legally while strengthening your overall financial health.

Tip: The best time to reduce your taxes legally is not when you file your Income Tax Return—it is when the financial year begins.

Frequently Asked Questions (FAQs)

1. How can I reduce my income tax legally in 2026?

You can legally reduce your income tax by choosing the appropriate tax regime, claiming eligible deductions and exemptions, planning capital gains, investing according to your financial goals, maintaining proper records, and filing your Income Tax Return accurately and on time.

2. Which tax regime is better in 2026 – Old or New?

There is no single answer. The Old Tax Regime may benefit taxpayers claiming substantial deductions such as Section 80C, 80D, HRA, and home loan interest, whereas the New Tax Regime may be more suitable for taxpayers with limited deductions. Always calculate your tax liability under both regimes before making a decision.

3. Is tax planning legal in India?

Yes. Tax planning is completely legal. The Income-tax Act provides several deductions, exemptions, rebates and incentives that taxpayers can legitimately use to reduce their tax liability. However, tax evasion through concealment of income or false claims is illegal.

4. Should I invest only to save income tax?

No. Tax saving should never be the sole reason for making an investment. Investments should first support your long-term financial goals such as retirement planning, wealth creation or financial security. Tax benefits should be considered an additional advantage.

5. What are the most common mistakes taxpayers make while planning taxes?

Common mistakes include choosing the wrong tax regime, investing at the last minute, failing to report all sources of income, ignoring the Annual Information Statement (AIS), claiming deductions without proper documentation, and filing the Income Tax Return after the due date.

6. Is it necessary to check AIS before filing my Income Tax Return?

Yes. The Annual Information Statement (AIS) contains information about your salary, bank interest, dividends, securities transactions, TDS and other financial transactions. Reconciling your return with AIS helps reduce the possibility of receiving tax notices due to mismatches.

7. Can I reduce tax on capital gains legally?

Yes. Proper planning before selling an asset can help reduce capital gains tax. Depending on the nature of the asset and applicable legal provisions, exemptions or reinvestment benefits may be available. Always evaluate the tax implications before completing the sale.

8. Why should I start tax planning at the beginning of the financial year?

Early tax planning allows you to spread investments throughout the year, improve cash flow, avoid last-minute financial decisions and maximise available tax-saving opportunities. It also reduces the risk of missing important deductions.

9. What documents should I preserve for income tax purposes?

You should retain Form 16, AIS, Form 26AS, investment proofs, medical insurance receipts, home loan certificates, bank statements, capital gains records, donation receipts and other supporting documents relating to deductions and income reported in your Income Tax Return.

10. Can I prepare my own Income Tax Return without professional help?

Yes, if your income and tax affairs are straightforward. However, if you have multiple sources of income, capital gains, business or professional income, foreign assets, or complex deductions, consulting a qualified tax professional can help ensure accurate compliance and effective tax planning.

11. Can AI help me with tax planning and Income Tax Return filing?

Artificial Intelligence (AI) can assist in understanding tax provisions, organising information and preparing draft content. However, taxpayers should always verify legal provisions, review calculations carefully and rely on official sources or qualified professionals before filing their Income Tax Return.

Disclaimer

This publication is intended solely for informational and educational purposes and does not constitute professional, legal, tax, or financial advice. The information provided has been compiled from sources believed to be reliable; however, its accuracy, completeness, or current relevance is not guaranteed. The views and opinions expressed herein reflect the author’s understanding at the time of publication and are subject to change without notice.

Readers are strongly advised to seek independent professional advice before making any decision or taking any action based on the information contained in this publication. The author and publisher expressly disclaim any responsibility or liability for any loss, damage, or consequence arising directly or indirectly from reliance on this content or from any action taken or not taken based on it.