Paid GST… still lost ITC?

Imagine doing everything right—verified supplier, genuine invoice, GST paid through bank—and still receiving a GST notice saying “ITC denied because your supplier didn’t deposit tax.”

Sounds unfair?

In 2026, High Courts across India finally agreed with taxpayers. In a series of strong judgments, courts ruled that bona-fide buyers cannot be punished for the supplier’s default.

If you’re a genuine businessperson who paid GST, booked invoices correctly, and still lost ITC because the supplier messed up, you’re not alone.

And more importantly, High Courts are finally saying this is unfair.

Brief Legislative Background (Why this problem even started)

When GST came in, the idea was simple:

- Buyer gets Input Tax Credit (ITC)

- Supplier pays tax to the Government

- Everyone stays compliant

But then came Section 16(2)(c) of the CGST Act, which says:

ITC is allowed only if tax charged has actually been paid to the Government by the supplier.

On paper, this looks logical.

In reality? Buyers were punished for mistakes they never committed.

Overview of Statutory Provisions Interpreted

The courts mainly examine

Section 16(2)(c), CGST Act

- Makes buyer’s ITC dependent on supplier’s tax payment

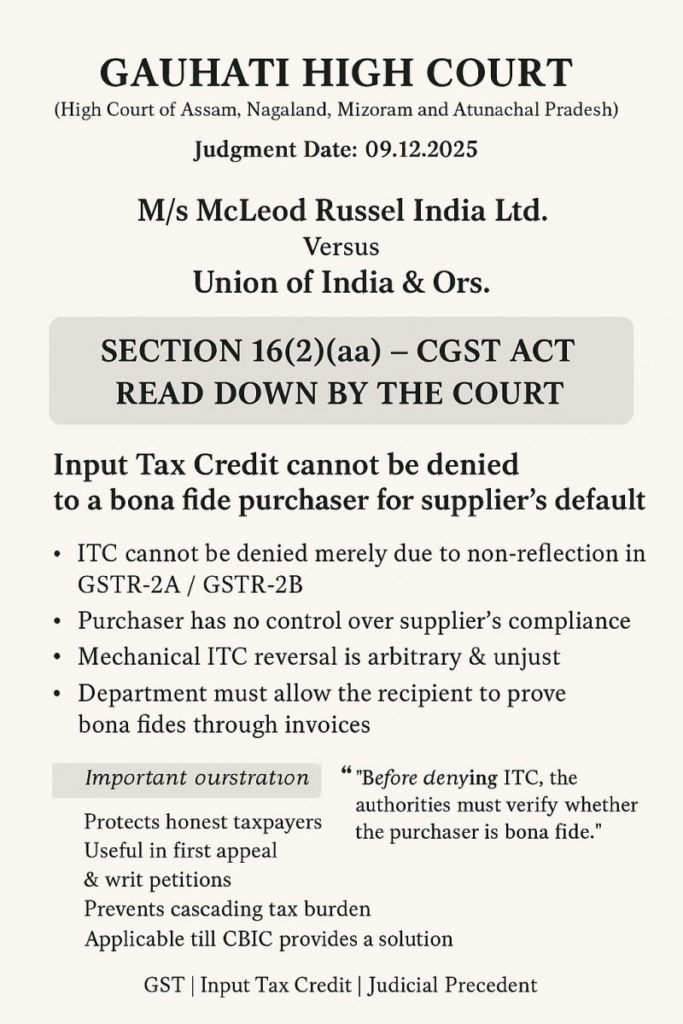

Section 16(2)(aa)

- Invoice must be reflected in GSTR-2B

Principles of Natural Justice

- You cannot penalize someone without fault

- Law should be reasonable, not oppressive

Detailed Analysis of the Judgments (What Courts Actually Said)

🏛 Tripura High Court – Sahil Enterprises v. Union of India

This judgment was a turning point.

The Court said (in simple words):

- A genuine buyer cannot control whether supplier deposits GST

- Government has full machinery to recover tax from supplier

- Denying ITC to buyer is arbitrary and unconstitutional

👉 Result: Section 16(2)(c) was read down to protect bona-fide buyers.

🏛 Kerala High Court – Santhom Metacast (P.) Ltd.

Kerala HC echoed the same logic:

- Buyer fulfilled all conditions

- Payments made through banking channels

- No allegation of fraud or collusion

👉 ITC denial was held unsustainable.

🏛 Calcutta High Court – Anjita Dokania

This case strengthened the taxpayer’s position:

- Authorities must first act against defaulting supplier

- Buyer should not be the “easy target”

Comparative Analysis with Earlier Judgments

❌ Earlier approach

- “Law is law, ITC depends on supplier”

- Mechanical denial of credit

- No inquiry into buyer’s conduct

Current judicial trend (2025–26)

- Focus on bona-fide conduct

- Distinction between fraud cases and genuine cases

- Constitutional interpretation of GST provisions

Clear shift from rigid compliance to fairness

Interpretation of Provisions Considering Judicial Rulings

Courts are effectively saying:

“Section 16(2)(c) cannot be applied blindly.”

What this means practically:

- If buyer is genuine → ITC should not be denied

- Department must:

- Investigate supplier

- Prove collusion, if any

- Burden cannot be automatically shifted to buyer

Core Principles Emerging from These Judgments

Let me sum this up simply:

✔ GST is destination-based, not punishment-based

✔ Law should encourage compliance, not fear

✔ Bona-fide taxpayers deserve protection

✔ Department must use recovery powers wisely

✔ Mechanical ITC denial will not survive judicial scrutiny

Practical Implications for Directors & Companies

✅ What businesses should do now:

- Maintain clean vendor documentation

- Pay suppliers through bank only

- Regularly reconcile GSTR-2B

- Avoid suspicious or non-compliant vendors

💼 For Directors:

- These rulings are a huge relief

- Personal exposure reduces if compliance is genuine

- Strong defense available during audits & SCNs

The Way Forward (My honest view)

GST law is evolving—and courts are bringing balance.

What I expect next:

- Clear CBIC clarification

- Structured mechanism to recover tax from suppliers

- Less harassment of genuine buyers

- Litigation to reduce over time

Until then, these judgments are your shield.

If you’ve done your job honestly,

the law should not make you suffer for someone else’s mistake—and finally, courts agree.

This is not tax evasion protection.

This is taxpayer dignity.

FAQ :-

FAQ 1: Can GST ITC be denied if the supplier fails to pay tax?

Earlier, tax officers routinely denied ITC under Section 16(2)(c) of the CGST Act.

However, High Courts in 2025–26 have clearly held that ITC cannot be denied to a bona-fide buyer who has:

- Received goods/services

- Paid GST to the supplier

- Maintained proper documentation

FAQ 2: What does “bona-fide buyer” mean in GST law?

A bona-fide buyer is one who:

- Purchases from a genuine supplier

- Makes payment through banking channels

- Records invoices properly

- Reflects ITC in GSTR-2B

- Is not involved in fraud or collusion

If these conditions are met, courts say ITC should not be denied.

FAQ 3: What did High Courts say about Section 16(2)(c)?

Courts held that:

- Section 16(2)(c) cannot be applied mechanically

- Buyer cannot be expected to ensure supplier’s tax payment

- Department must first proceed against defaulting supplier

- Denial of ITC without buyer’s fault is arbitrary and unfair

FAQ 4: Does this relief apply in cases of fake invoices or fraud?

❌ No.

These judgments do not protect fraudulent transactions.

Relief applies only to genuine transactions where:

- Goods/services are real

- Supplier exists

- No evidence of collusion or fake invoicing

FAQ 5: How should businesses protect their GST ITC after these rulings?

Businesses should:

- Conduct vendor due diligence

- Avoid suspicious suppliers

- Maintain payment proof

- Regularly reconcile GSTR-2B

- Respond promptly to GST notices

Disclaimer

This publication is intended solely for informational and educational purposes and does not constitute professional, legal, tax, or financial advice. The information provided has been compiled from sources believed to be reliable; however, its accuracy, completeness, or current relevance is not guaranteed. The views and opinions expressed herein reflect the author’s understanding at the time of publication and are subject to change without notice.

Readers are strongly advised to seek independent professional advice before making any decision or taking any action based on the information contained in this publication. The author and publisher expressly disclaim any responsibility or liability for any loss, damage, or consequence arising directly or indirectly from reliance on this content or from any action taken or not taken based on it.