Many citizens submit financial forms annually. Slight oversights often trigger unwanted scrutiny or cause refunds to stay stagnant. The Department now employs a quick programme for catching minor errors.

Mismatches in AIS/TIS data points lead to increased observation. Even misspelt names or wrong bank details lead to big delays. “A small error today can become a big tax problem tomorrow.”

The groups started large awareness campaigns, helping people navigate these hurdles. Staying diligent ensures a seamless experience with revenue services nationwide. Taking care now prevents future stress and potential penalties from legal bodies.

Accuracy remains the most vital part of the entire submission journey for everyone. Professionals suggest double-checking every single figure before clicking the final button on the portal. This simple habit keeps one safe from formal notices and unnecessary headaches.

Key Takeaways

- Rectify AIS/TIS mismatches promptly.

- Verify bank account numbers before submission.

- Double-check name spellings for accuracy.

- Understand automated department processing systems.

- Utilise pre-filing awareness campaign resources.

- Prioritise data accuracy for faster refunds.

Why Accuracy Matters in Income Tax Return Filing: Mistakes to Avoid in 2026

Filing an incorrect return can lead to delays, penalties, and even legal implications. It is essential for taxpayers to understand the potential consequences of errors in their income tax return filing.

- Increased use of AIS (Annual Information Statement)

- Real-time data matching (banks, brokers, GST, etc.)

- Faster processing & automated notices

- Strict compliance monitoring

👉 Accuracy is no longer optional — it is essential.

The Financial and Legal Implications of Errors

Errors in income tax return filing can result in significant financial implications, including penalties and interest on the tax owed. In severe cases, it can also lead to legal action against the taxpayer.

The financial implications of errors can be broken down into several key areas:

- Penalties for incorrect or late filing

- Interest on the tax owed

- Potential for legal action

Understanding the Role of the Annual Information Statement (AIS)

The Annual Information Statement (AIS) plays a crucial role in tax filing, providing a comprehensive view of a taxpayer’s financial transactions. Understanding its significance is vital for compliant tax filing.

AIS includes information such as:

- Details of high-value transactions

- Dividend income

- Interest income

- Other financial transactions

Taxpayers must ensure that the information in their AIS is accurate and reflects their actual financial transactions.

To avoid common tax filing errors, taxpayers should be aware of the top 15 income tax return filing mistakes to avoid. By understanding the financial and legal implications of errors and the role of AIS, taxpayers can ensure accurate and compliant tax filing.

Reporting and Documentation Errors

Reporting and documentation errors are common pitfalls that can delay or complicate the income tax return process. Taxpayers must be vigilant in ensuring that all information is accurately reported and supported by the necessary documentation.

Many taxpayers forget to include:

- Interest from savings accounts & FDs

- Freelance or side income

- Rental income

- Capital gains from shares or property

👉 Even ₹1 mismatch can trigger a notice.

One of the most common issues arises from discrepancies between the information provided by employers and what is reflected in the tax returns. Mismatches Between Salary Slips and Form 16 can lead to notices from the tax authorities, as these documents are critical in verifying income.

Mismatches Between Salary Slips and Form 16

A mismatch occurs when the figures on the salary slip do not align with those on Form 16. This discrepancy can be due to various reasons, such as incorrect reporting of salary components or failure to update records. To avoid this, taxpayers should ensure that their salary slips and Form 16 are consistent and accurately reflect their income.

Failing to Report Exempt Income and Foreign Assets

Taxpayers often overlook reporting exempt income and foreign assets, which can lead to complications. It is essential to understand what constitutes exempt income and to report it correctly. Similarly, foreign assets must be declared, even if they are not taxable in India, to comply with global reporting standards.

Failing to report these can result in penalties and unnecessary scrutiny. Taxpayers should be aware of the requirements and ensure compliance to avoid an income tax notice.

Foreign Income

Includes:

- Salary earned abroad

- Foreign investments income

- Dividend/interest from overseas

Requirement:

👉 Must be reported in:

- Schedule FSI (Foreign Source Income)

- Claim relief under DTAA if applicable

❌ Common Mistake:

👉 Ignoring foreign income assuming it is taxed abroad

Foreign Assets

Includes:

- Foreign bank accounts

- Shares in foreign companies

- Property outside India

Requirement:

👉 Must be reported in Schedule FA

Risk:

- Severe penalties

- Action under Black Money Act

Exempt Income

Examples:

- Agricultural income

- PPF interest

- Certain dividends

- Tax-free bonds

Common Mistake:

👉 Not reporting exempt income at all

Agricultural Income

Key Point:

- Agricultural income is exempt from tax

- But must be reported in ITR

Why Reporting is Important:

- Used for rate calculation (partial integration)

- Helps department verify source of funds

❌ Common Mistake:

👉 Not reporting agricultural income at all

💥 Why Non-Reporting is Dangerous

- AIS captures multiple transactions

- Department cross-verifies income sources

- Non-reporting may lead to:

- Notice

- Scrutiny

- Penalty

Real-Life Scenario

👉 Mr. A received ₹3 lakh agricultural income

- Did not report it ❌

👉 Result:

- Income mismatch noticed

- Asked to explain source

How to Avoid This Mistake

✔ Report all income — taxable or exempt

✔ Disclose foreign income/assets properly

✔ Maintain documentation

✔ Check AIS carefully

✔ Understand disclosure schedules in ITR

Incorrect Personal Details and Bank Account Validation

Incorrect personal details, such as name, date of birth, or PAN, can delay the processing of tax returns. Moreover, incorrect bank account details can delay the refund process. It is crucial to ensure that all personal and bank account details are accurate and validated.

By being meticulous in reporting and documentation, taxpayers can significantly reduce the risk of errors and subsequent notices from the tax authorities. Ensuring accuracy and compliance in these areas is key to a smooth and efficient tax filing process.

Deduction and Tax Calculation Pitfalls

The process of claiming deductions and calculating tax liabilities is fraught with potential pitfalls that can lead to significant financial implications. Taxpayers must be aware of the rules and regulations surrounding deductions and tax calculations to ensure compliance.

Claiming Ineligible Deductions Under Old and New Regimes

Taxpayers often mistakenly claim deductions under the old and new tax regimes without understanding the eligibility criteria. It is essential to familiarise oneself with the deductions available under each regime to avoid claiming ineligible deductions.

For instance, under the old regime, taxpayers can claim deductions for investments in certain savings schemes and expenses like medical insurance premiums. However, under the new regime, such deductions are not available. A clear understanding of these differences can help taxpayers avoid errors.

You can also read a detailed blog on Income Tax Slabs 2026: Old vs New Regime – Smart Tax Tips

Double-Dipping on Tax Exemptions

Double-dipping occurs when taxpayers claim the same exemption or deduction multiple times. This can happen when taxpayers fail to understand the nuances of tax laws or misinterpret the provisions.

For example, claiming a deduction for the same investment or expense under different sections of the Income Tax Act is considered double-dipping. Taxpayers must ensure that they do not claim duplicate exemptions to avoid penalties.

Errors in Calculating Taxable Income Slabs

Calculating taxable income slabs correctly is crucial to avoid errors in tax calculations. Taxpayers must accurately determine their total income and apply the correct tax rates as per the prevailing tax slabs.

A common mistake is miscalculating the taxable income by incorrectly claiming deductions or exemptions, leading to incorrect tax liability. Using an ITR filing checklist can help taxpayers ensure that they have considered all relevant factors.

| Common Mistakes | Consequences | Prevention |

|---|---|---|

| Claiming ineligible deductions | Penalties and interest on tax due | Familiarise yourself with eligible deductions under each tax regime |

| Double-dipping on tax exemptions | Tax notices and potential penalties | Understand tax laws and claim exemptions correctly |

| Errors in calculating taxable income slabs | Incorrect tax liability and potential penalties | Accurately calculate total income and apply correct tax rates |

Capital Gains and Investment Reporting Blunders

Mistakes in reporting capital gains and investments can have significant consequences, making it essential to understand the common errors.

When taxpayers invest in assets such as stocks, real estate, or mutual funds, they must report any gains or losses from these investments on their income tax returns. The process involves understanding the nuances of capital gains tax, including the distinction between short-term and long-term gains, the impact of indexation, and the reporting of off-market transactions.

👉 To understand taxation of assets in detail, read our

complete capital gains tax guide for India 2026 Guide: Capital Gains Tax on Shares, Funds & Property

Misclassifying Short-Term and Long-Term Capital Gains

One common mistake is misclassifying short-term and long-term capital gains. The period of holding an asset determines whether the gain is short-term or long-term, with different tax implications for each.

One of the most common and serious mistakes while filing ITR is wrong classification of capital gains as Short-Term (STCG) or Long-Term (LTCG).

👉 This directly impacts:

- Tax rate

- Exemptions

- Final tax liability

📊 What is the Difference?

🔹 Short-Term Capital Gain (STCG)

- Gain from assets held for short duration

- Generally taxed at higher rates

- Less than 24 months( other than listed shares) → STCG, taxed on slab rates

- Less than 12 months( listed shares) → STCG (Tax ~20%)Section 111A

🔹 Long-Term Capital Gain (LTCG)

- Gain from assets held for longer period

- Taxed at lower rates + exemptions available

- More than 24 months (others) → LTCG taxed @ 12.5%

- More than 12 months( listed shares) → LTCG (Tax ~12.5% above ₹1.25 lakh)for Section 112A

Now mostly taxed as short-term (as per slab rates)

Indexation benefit largely removed (for new investments)

Common Mistakes Taxpayers Make

❌ Treating long-term gains as short-term (paying excess tax)

❌ Treating short-term gains as long-term (risk of notice)

❌ Ignoring holding period calculation

❌ Mixing up asset categories

❌ Not considering grandfathering rules (equity before 31 Jan 2018)

💥 Why This Mistake is Dangerous

- Wrong tax calculation

- Notice from Income Tax Department

- Interest & penalty

- Scrutiny risk

👉 AIS and broker reports make detection easy in 2026

💡 Practical Example

👉 Mr. A sold shares after 10 months

- Declared as LTCG ❌

- Actual: STCG

👉 Result:

- Underpaid tax

- Received notice

- Paid additional tax + penalty

How to Avoid This Mistake

✔ Always check purchase & sale date

✔ Use broker capital gain statement

✔ Classify asset correctly

✔ Cross-check with AIS

✔ Take professional help if needed

Ignoring Off-Market Transactions and Gift Reporting

Taxpayers often overlook reporting off-market transactions and gifts, which can lead to unreported income and potential tax liabilities. Off-market transactions, such as transferring securities without a broker, must be reported accurately.

Many taxpayers believe that only stock market or bank transactions matter for ITR filing.

However, off-market transactions and gifts are equally important and often reported in AIS/TIS.

👉 Ignoring them can lead to notices, tax demands, or penalties.

What are Off-Market Transactions?

Off-market transactions are those where assets are transferred without using stock exchange platforms.

Common Examples:

- Transfer of shares between family members

- Gift of shares or mutual funds

- Transfer of unlisted shares

- Private sale of assets (without exchange)

👉 These transactions may still appear in AIS or broker reports.

Gift Transactions – Tax Implications

Gifts from Relatives

👉 Fully tax-free

(Relatives include: spouse, parents, siblings, etc.)

Gifts from Non-Relatives

👉 Taxable if value exceeds ₹50,000 in a year

👉 Taxed under “Income from Other Sources”

Common Mistakes Taxpayers Make

❌ Not reporting gifted shares or money

❌ Ignoring off-market share transfers

❌ Assuming “gift = no tax always”

❌ Not maintaining gift deed/documentation

❌ Not reporting sale of gifted assets later

Why This Mistake is Dangerous

- AIS reflects high-value transactions

- Income Tax Department may question source

- Tax + penalty exposure

- Risk of scrutiny

👉 Especially important in 2026 due to enhanced data tracking

Special Point: Sale of Gifted Assets

👉 Very important concept:

- Cost of acquisition = cost of previous owner

- Holding period = includes previous owner’s period

👉 Wrong reporting here can lead to:

- Incorrect capital gains

- Notice from department

Practical Example

👉 Mr. B received shares worth ₹2 lakh from a friend

- Not reported in ITR ❌

- Exceeds ₹50,000

👉 Result:

- Taxable income added

- Notice received

How to Avoid This Mistake

✔ Report all gifts (if taxable)

✔ Maintain proper gift documentation

✔ Check AIS carefully

✔ Report sale of gifted assets correctly

✔ Understand relative vs non-relative rules

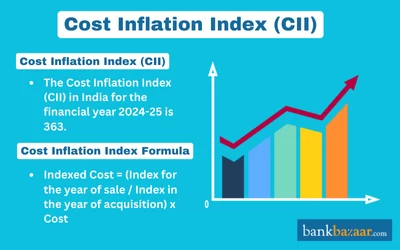

Forgetting to Adjust for Indexation Benefits

Forgetting to adjust for indexation benefits when calculating long-term capital gains can result in higher tax liabilities. Indexation adjusts the purchase price of an asset for inflation, reducing the taxable gain.

Tip: Taxpayers should keep records of the cost inflation index to correctly calculate the indexed cost of acquisition.

By understanding these common blunders in capital gains and investment reporting, taxpayers can ensure compliance with tax regulations and avoid potential penalties.

Basic Formula

👉 Indexed Cost of Acquisition = Cost of Purchase×CII of Sale YearCII of Purchase Year\text{Cost of Purchase} \times \frac{\text{CII of Sale Year}}{\text{CII of Purchase Year}}Cost of Purchase×CII of Purchase YearCII of Sale Year

Where is Indexation Applicable?

✔ Allowed:

- Real estate (land/building)

- Certain long-term capital assets purchased before 23 rd July 2024

❌ Not Allowed:

- Equity shares

- Equity mutual funds

⚠️ Important Update:

- Debt mutual funds (recent investments)

👉 Indexation benefit mostly removed

Common Mistakes Taxpayers Make

❌ Not applying indexation where allowed

❌ Using wrong CII numbers

❌ Applying indexation to assets where not allowed

❌ Ignoring year of acquisition rules

❌ Incorrect calculation in inherited/gifted assets

Why This Mistake is Dangerous

- Incorrect tax liability

- Excess tax payment (very common)

- Scrutiny in high-value transactions

- Errors easily detectable through AIS/property data

Practical Example

👉 Purchase Price (2010): ₹10 lakh

👉 Sale Price (2025): ₹30 lakh

Without indexation:

👉 Gain = ₹20 lakh

With indexation:

👉 Indexed Cost ≈ ₹20 lakh

👉 Gain = ₹10 lakh

👉 Huge tax saving!

How to Avoid This Mistake

✔ Always check CII values

✔ Apply indexation where allowed

✔ Use correct formula

✔ Take expert help for property transactions

✔ Verify calculations before filing

Tax Credit and TDS Discrepancies

One of the most common pitfalls in ITR filing concerns tax credit and TDS discrepancies. Taxpayers must ensure that their tax credits and TDS are accurate to avoid unnecessary notices and penalties from the tax authorities.

- TDS = Tax deducted by the employer/bank before payment

- Tax Credit = Amount reflected in your Form 26AS / AIS

👉 You can claim only the TDS actually appearing in records

Common Mistakes Taxpayers Make

❌ Claiming excess TDS not reflected in Form 26AS

❌ Ignoring missing TDS entries

❌ Not checking AIS before filing

❌ Mismatch between Form 16 and 26AS

❌ Entering incorrect TAN or amount

Why This Mistake is Critical

- ITR is processed based on system data (26AS/AIS)

- If mismatch occurs:

👉 Refund may be reduced

👉 Tax demand may be raised

Typical Real-Life Scenarios

🔹 Case 1: Missing TDS Entry

- Bank deducted TDS

- Not deposited or not reflected

👉 You claim it → system rejects

🔹 Case 2: Form 16 vs 26AS Mismatch

- Employer shows TDS

- But not uploaded correctly

👉 Leads to discrepancy

🔹 Case 3: Wrong TDS Claimed

- Typing error

- Double claim

👉 Immediate mismatch notice

How to Avoid TDS Discrepancies

✔ Always download Form 26AS before filing

✔ Cross-check with:

- Form 16 (salary)

- Form 16A (other income)

✔ Match every entry carefully

✔ Report only verified TDS

✔ Follow up with deductor if mismatch exists

What to Do If a Mismatch Exists?

👉 Before filing:

- Contact employer/bank to correct TDS return

👉 After filing:

- File rectification request

- Or revise return

Discrepancies Between Form 26AS and Actual TDS Deducted

A common issue taxpayers face is the discrepancy between the TDS credit reflected in Form 26AS and the actual TDS deducted by the employer or deductor. This mismatch can occur due to incorrect PAN details, delayed TDS deposits by the deductor, or other administrative errors.

Why This Happens

🔹 1. TDS Not Deposited by Deductor

- Employer/bank deducted tax

- But failed to deposit with government

🔹 2. Delay in Filing TDS Return

- TDS deposited

- But return not filed yet

🔹 3. Incorrect Details Filed

- Wrong PAN entered

- Incorrect amount reported

🔹 4. Timing Difference

- TDS deducted near year-end

- Appears later in 26AS

💥 Impact on Taxpayer

❌ Cannot claim full TDS credit

❌ Refund gets reduced

❌ Tax demand may arise

❌ Delay in ITR processing

📌 Practical Example

👉 Mr. A’s employer deducted ₹80,000 TDS

👉 Form 26AS shows only ₹60,000

👉 He claimed full ₹80,000 ❌

👉 Result:

- ₹20,000 disallowed

- Demand raised

✅ What Should You Do?

✔ Before Filing ITR

- Always check Form 26AS

- Match with:

- Form 16 (salary)

- Form 16A (other income)

✔ If Mismatch Exists

👉 Contact deductor (employer/bank)

Ask them to:

- Deposit TDS (if not done)

- Revise TDS return

✔ If Already Filed ITR

👉 Options:

- File revised return (after correction)

- Or apply for rectification

⚠️ Important Rule

👉 You can claim only that TDS which is reflected in Form 26AS

💡 Pro Tip

“Do not rush to file ITR — wait until your Form 26AS is fully updated.”

Failing to Claim Credits for Taxes Paid Abroad

Taxpayers who have paid taxes abroad on their foreign income may be eligible to claim a credit on their Indian income tax return. Failing to claim this credit can result in double taxation of the same income, increasing tax liability.

To claim this credit, taxpayers need to furnish details of the foreign income and the taxes paid on it. It is advisable to maintain proper documentation, including certificates of foreign tax credit, to support the claim.

Overlooking Advance Tax Payments

Advance tax payments, also known as “pay as you earn,” are crucial for taxpayers with income that is not subject to TDS, such as self-employed individuals or those with significant investment income. Overlooking these payments or failing to pay the correct amount can lead to interest liabilities under sections 234B and 234C of the Income Tax Act.

Taxpayers should calculate their advance tax liability accurately and make timely payments to avoid any penalties or interest. It is also essential to keep track of the advance tax payment due dates to ensure compliance.

👉 To understand how TDS impacts your tax liability, read our

Advance tax rules and due dates in India Advance Tax

Compliance and Procedural Oversights

Ensuring compliance with tax regulations is crucial to avoid penalties and notices from tax authorities. Taxpayers must be aware of the common compliance and procedural oversights that can lead to complications during the income tax return filing process.

Selecting the Wrong ITR Form

One of the most common mistakes taxpayers make is selecting the incorrect Income Tax Return (ITR) form. The Indian Income Tax Department offers different ITR forms for different types of taxpayers based on their income sources and taxpayer status. Choosing the wrong form can delay processing or even result in a notice from the tax authorities.

For instance, ITR-1 (Sahaj) is for individuals with income from salaries, one house property, and other sources. If an individual has income from multiple house properties or capital gains, they must file a different form, such as ITR-2 or ITR-3. Ensuring the correct form is used is the first step towards a smooth filing process.

| ITR Form | Eligible Taxpayers | Income Sources Covered |

|---|---|---|

| ITR-1 (Sahaj) | Individuals & HUFs | Salary, one house property, other sources |

| ITR-2 | Individuals & HUFs | Salary, multiple house properties, capital gains |

| ITR-3 | Individuals & HUFs | Business or professional income, along with other sources |

Neglecting Mandatory E-Verification

After filing the income tax return, e-verification is a mandatory step that verifies the authenticity of the return. Neglecting this step can result in the return being deemed invalid by the tax authorities. E-verification can be done through various methods, including Aadhaar OTP, net banking, or by sending a signed physical copy (ITR-V) to the CPC.

It is essential to complete the e-verification process within the stipulated time frame (usually 30 days) to avoid any complications.

Missing Deadlines and the Penalty for Late Filing

Missing the deadline for filing income tax returns can result in penalties and additional tax liabilities. The due date for filing ITRs is typically July 31st for individuals; failing to file by this date may attract a penalty under Section 234F of the Income Tax Act. Nominal fees on filing revised ITR from January to March under Section 243I

The penalty for late filing can be up to ₹5,000 for individuals. Moreover, delayed filing can also result in the loss of certain benefits, such as carrying forward losses.

To avoid these compliance and procedural oversights, taxpayers should be diligent in selecting the correct ITR form, ensure timely e-verification, and file their returns before the deadline. By doing so, they can ensure a smooth and hassle-free income tax filing experience.

Emerging Challenges and New Mistakes in 2026

As we approach 2026, taxpayers must be aware of the emerging challenges in the tax landscape. The tax environment is becoming increasingly complex, with new regulations and requirements being introduced regularly.

Taxpayers need to stay informed about these changes to avoid making costly mistakes in their income tax return filings. Some of the key areas of concern include digital asset taxation, gig economy income, and high-value transactions.

Navigating Changes in Digital Asset Taxation

The taxation of digital assets is becoming a significant area of focus for tax authorities. Taxpayers who invest in or trade digital assets, such as cryptocurrencies, need to understand the tax implications of these investments.

- Taxpayers must report gains or losses from the sale of digital assets in their income tax returns.

- The tax treatment of digital assets can vary depending on the type of asset and the taxpayer’s jurisdiction.

- It is essential to maintain accurate records of digital asset transactions to ensure compliance with tax regulations.

Reporting Income from the Gig Economy and Freelancing

The gig economy and freelancing are becoming increasingly popular, and taxpayers who earn income from these sources need to understand their tax obligations.

Taxpayers must report their gig economy and freelancing income on their income tax returns, and they may be eligible for deductions on business expenses related to this income.

Key considerations for gig economy and freelancing income include:

- Accurate record-keeping of income and expenses.

- Understanding the tax treatment of different types of gig economy and freelancing income.

- Claiming eligible deductions and allowances.

New Reporting Requirements for High-Value Transactions

Tax authorities are introducing new reporting requirements for high-value transactions to combat tax evasion and money laundering.

Taxpayers who engage in high-value transactions, such as property purchases or large cash transactions, need to be aware of these new requirements and ensure compliance.

High-value transactions are large financial activities automatically reported to the Income Tax Department by banks and institutions.

👉 These appear in:

- AIS

- Form 26AS (Part E)

Common High-Value Transactions Tracked

💰 Banking Transactions

- Cash deposit ≥ ₹10 lakh (savings account) if you have a PAN Number

- Cash deposit ≥ ₹5 lakh (savings account) if you do not have a PAN Number

- Cash deposit/withdrawal ≥ ₹50 lakh (current account)

- Borrow and repay a loan or security deposit in cash ≥20 Thousand

🏠 Property Transactions

- Purchase/sale of property ≥ ₹30 lakh reported to IT Department

💳 Credit Card Transactions

- Large payments (especially ₹10 lakh+ annually) tracked

📊 Investments

- Mutual funds, shares, bonds above thresholds

- Fixed deposits ≥ ₹10 lakh

💵 Cash Transactions

- Cash receipt ≥ ₹2 lakh restricted under law

- Cash expenses per day to a person should not be ≥10 thousand

Common Mistakes Taxpayers Make

❌ Ignoring AIS entries of high-value transactions

❌ Not reporting income related to such transactions

❌ Assuming “bank transactions need not be reported”

❌ Not reconciling property or investment transactions

❌ Mismatch between lifestyle and declared income

Why This Mistake is Dangerous

- Transactions are automatically reported by banks, registrars, MF houses

- Even if you don’t disclose, department already knows

- Mismatch triggers:

- E-campaign notices

- Scrutiny

- Reassessment

👉 High-value transactions are a key trigger for income tax notices

Real-Life Scenario

👉 Mr. X deposited ₹15 lakh in cash

- Did not report corresponding income ❌

👉 Result:

- AIS reflected transaction

- Notice received

- Asked to explain source of funds

How to Avoid This Mistake

✔ Always check AIS before filing ITR

✔ Reconcile all high-value transactions

✔ Report income properly (salary/business/capital gains)

✔ Maintain supporting documents

✔ Ensure your income justifies your lifestyle

By understanding these emerging challenges and new reporting requirements, taxpayers can ensure compliance with tax regulations and avoid costly mistakes in their income tax return filings.

Consequences of Filing Incorrect Returns

Taxpayers in India must be aware of the potential consequences of filing incorrect returns. Filing an incorrect income tax return can lead to a range of issues, from financial penalties to legal complications.

Filing an incorrect Income Tax Return is not just a small mistake — it can lead to serious financial and legal consequences.

With advanced data tracking through AIS, Form 26AS, and automated systems, errors are quickly identified in 2026.

1. Income Tax Notices

If discrepancies are found, you may receive notices such as:

- Section 143(1) – Intimation for mismatch

- Section 139(9) – Defective return

- Section 148 – Reassessment notice

👉 Even small mismatches can trigger automated notices.

2. Additional Tax Liability

- Underreported income → extra tax demand

- Incorrect claims → reversal of deductions

👉 You may have to pay additional tax along with interest

3. Interest Liability

Interest may be charged under:

- Section 234A – Delay in filing

- Section 234B – Default in advance tax

- Section 234C – Delay in installments

👉 This increases your overall tax burden significantly.

4. Penalties

Depending on the nature of error:

- Late filing penalty (Section 234F)

- Penalty for under-reporting/misreporting of income

👉 Penalties can be substantial in serious cases.

5. Delay in Refund

- Mismatch in TDS or income

- Incorrect bank details

👉 Leads to:

- Refund hold

- Reduced refund

- Processing delays

6. Scrutiny or Assessment

Serious discrepancies may lead to:

- Detailed scrutiny of return

- Request for documents

- Income verification

👉 This can be time-consuming and stressful.

7. Reassessment Proceedings

If income is believed to have escaped assessment:

👉 Department can reopen your case

👉 Even past years can be reviewed (subject to law)

8. Loss of Tax Benefits

- Incorrect filing may lead to:

- Loss of deductions

- Loss of exemptions

- Inability to carry forward losses

9. Legal Consequences (In Serious Cases)

- In cases of deliberate misreporting:

- Heavy penalties

- Possible prosecution

👉 Especially in high-value or fraudulent cases

Real-Life Example

👉 A taxpayer failed to report stock market gains

- Received notice

- Paid additional tax + interest

- Faced scrutiny

👉 Lesson: Transparency is critical.

How to Stay Safe

✔ Report all income accurately

✔ Match AIS and Form 26AS

✔ Verify deductions properly

✔ File and verify ITR on time

✔ Revise return if any mistake is found

What Happens if a Mistake is Detected by the Department?

If the income tax department detects a mistake in your return, you may receive a notice or intimation. This could be in the form of an email or a letter, prompting you to rectify the error or provide additional information.

The department may also initiate proceedings under various sections of the Income-tax Act, 1961, depending on the nature of the mistake. For instance, if the error is deemed to be a result of negligence or an attempt to evade tax, you might face penalties.

In 2026, with AIS, data analytics, and automated systems, the Income Tax Department can easily detect mismatches in your return.

👉 When a mistake is detected, the department follows a structured process — not immediate penalty.

📩 1. Initial Intimation or Notice

In most cases, the first step is communication, not punishment.

Common notices:

- Section 143(1) → Mismatch in income or tax

- Section 139(9) → Defective return

- E-Compliance / AIS notice → Clarification required

👉 This is your first opportunity to correct or explain

🔎 2. Comparison with AIS & 26AS

The department checks:

- Income declared vs AIS

- TDS claimed vs Form 26AS

- High-value transactions vs reported income

👉 Any mismatch triggers further action

💰 3. Tax Recalculation

If error is confirmed:

- Income is recomputed

- Additional tax is calculated

👉 Along with:

- Interest (234A, 234B, 234C)

⚠️ 4. Demand Notice

👉 You may receive a tax demand notice

This includes:

- Additional tax payable

- Interest amount

- Due date for payment

🔁 5. Option to Respond or Correct

You still have options:

✔ Accept and pay demand

✔ File revised/updated return

✔ Submit explanation online

👉 This stage is very important to act quickly

🔍 6. Scrutiny (If Required)

If discrepancy is serious:

- Case may be selected for scrutiny

- Detailed documents may be asked

👉 Examples:

- High-value transactions

- Large capital gains mismatch

🔁 7. Reassessment Proceedings

If income is believed to have escaped:

👉 Case may be reopened

👉 Department can examine past years (as per law)

🚫 8. Penalty & Legal Action (In Serious Cases)

If mistake is:

- Intentional

- Misreporting

- Fraud

👉 Then:

- Penalty may be imposed

- In extreme cases → prosecution

📌 Real-Life Flow (Simple Understanding)

👉 Mistake detected →

👉 Notice issued →

👉 Tax recalculated →

👉 You respond/pay →

👉 Case closed

(If not resolved → scrutiny/reassessment)

💡 Key Takeaway

“Detection of mistake does not mean punishment — but ignoring it can lead to serious consequences.”

✅ How to Handle Such Situations

✔ Respond within time

✔ Check AIS and documents carefully

✔ Correct mistake voluntarily

✔ Seek professional help if required

The Process and Limitations of Revising Your Return

Making a mistake in your Income Tax Return is not the end — the law provides an opportunity to revise and correct your return within a specified time limit.

👉 The key is to act quickly and within the permitted time frame.

Time Limit for Filing Original & Revised Return

🔹 Original Return (Section 139(1))

- ITR1 and ITR2 to be filed by 31st July (for individuals unless extended)

- ITR 3, ITR4, ITR5 returns; non-audit business cases or trusts will continue to file till 31st August

🔹 Revised Return (Section 139(5))

What is a Revised Return?

A revised return replaces your original ITR completely.

👉 It is not partial correction — it is a fresh return with corrected details.

👉 You can revise your ITR if:

- You made a mistake

- Missed income

- Claimed wrong deduction

⏳ Time Limit:

👉 Before 31st December of the assessment year

OR

👉 Before completion of assessment (whichever is earlier)

👉Now can do so up to 31st March with the payment of nominal fees‘

Important Understanding

👉 Earlier belief:

- “If original return is filed on time, revision is free anytime” ❌

👉 Current practical reality:

- Delay beyond December may attract additional cost

- Correction is allowed, but not without financial impact

Practical Scenario

👉 Case 1:

- Original return filed in July ✔

- Mistake found in February

👉 Action:

- Correction possible

- But may involve additional payment

👉 Case 2:

- Return not filed till March

👉 Action:

- Still possible to file

- But with late fee / additional tax burden

💡 Key Message for Readers

“Timely filing and timely revision can save you money — delays can make corrections costly.”

Common Situations Where Revision is Needed

- Forgot to report income (FD interest, capital gains)

- Claimed incorrect deduction

- TDS mismatch corrected later

- Wrong ITR form selected

- Any data entry error

Can You Revise Return Multiple Times?

👉 Yes, you can revise your return multiple times

(as long as it is within the time limit),now time available for revising returns from 31st December to up to March, with the payment of nominal fees

Important Points to Remember

- Revised return replaces original return completely

- Always verify revised return

- Late filing may restrict revision benefits

- Keep supporting documents ready

What If You Miss the Revision Deadline?

👉 You may:

- File updated return (Section 139(8A)) (with conditions)

- Pay additional tax + penalty

Updated Return (After Revision Deadline): Important Rule You Must Know Section 267 of Income Tax Act ,1961

If you miss the deadline for filing a revised return (i.e., 31st December of the assessment year), you still have an option to correct your return.

👉 You can file an Updated Return under Section 139(8A).

⏳ Time Limit

👉 An updated return can be filed up to 48 months from the end of the relevant assessment year.

💰 Additional Tax / Fees Applicable

👉 Filing an updated return is not free.

- You must pay:

- Additional tax

- Interest

- Additional amount (25% or 50%or 60% or 70% of tax + interest) depending on delay

⚠️ Important Clarification

👉 Even if you had:

✔ Filed your original return on time

✔ But later found a mistake after 31st December and now after 31stMarch( return revised between January to March with nominal fees)

👉 You cannot revise the return after 31st March now

👉 Instead, you must file an Updated Return (139(8A)), and:

❗ Additional tax/fees will be payable

📌 Practical Understanding

👉 Situation:

- Original ITR filed on time (July) ✔

- Mistake discovered in after March❌

👉 Action:

- Revised return not allowed

- File Updated Return

- Pay additional tax + applicable charges

💡 Key Takeaway

“Correction after December comes at a cost — so always review and revise your return before the deadline.”

Dealing with Income Tax Notices and Scrutiny

Receiving an income tax notice can be unsettling, but it’s essential to respond promptly and appropriately. If your return is selected for scrutiny, you may be required to provide detailed documentation and explanations.

Common Types of Income Tax Notices

Section 143(1) – Intimation Notice

- Issued after processing ITR

- Shows mismatch in:

- Income

- TDS

- Tax calculation

👉 Usually informational, but needs review

Section 139(9) – Defective Return

- Filed ITR is incomplete or incorrect

- Example:

- Wrong ITR form

- Missing details

👉 Must correct within specified time

Section 148 – Reassessment Notice

- Income has escaped assessment

👉 Requires detailed response and documentation

E-Campaign / Compliance Notice

- Based on AIS data

- Requests explanation for mismatch

👉 Increasingly common in 2026

Why You May Receive a Notice

- Income mismatch with AIS

- High-value transactions not explained

- Incorrect capital gains reporting

- TDS mismatch

- Sudden increase in income or investment

Step-by-Step Process to Handle Notices

Step 1: Stay Calm & Read Carefully

👉 Understand:

- Section under which notice is issued

- Nature of discrepancy

✔ Step 2: Check AIS, 26AS & Filed ITR

👉 Identify:

- Where mismatch occurred

- Whether error is genuine

✔ Step 3: Gather Documents

Keep ready:

- Form 16 / 16A

- Bank statements

- Investment proofs

- Capital gain statements

✔ Step 4: Respond Online

👉 Login to Income Tax Portal

👉 Submit response within deadline

✔ Step 5: Revise Return (If Required)

👉 If mistake found:

- File revised return

- Pay additional tax

✔ Step 6: Seek Professional Help (If Needed)

👉 Especially for:

- Reassessment

- Scrutiny cases

What Happens If You Ignore Notice?

❌ Additional tax demand

❌ Penalty & interest

❌ Scrutiny proceedings

❌ Legal consequences

👉 Ignoring is the worst option

Practical Example

👉 Mr. X received notice for mismatch in stock transactions

- Checked AIS

- Found missing capital gains

- Filed revised return

👉 Result:

✔ Issue resolved without penalty escalation

Pro Tips to Handle Notices Safely

✔ Always respond within time

✔ Do not ignore communication

✔ Keep documentation ready

✔ Be honest and transparent

✔ Take expert advice if unsure

Practical Checklist and Pro Tips for a Flawless Filing

Filing your Income Tax Return (ITR) can be a daunting task, but with a practical checklist, you can avoid common mistakes. Ensuring accuracy and compliance in your tax filing is crucial to avoid IT filing mistakes in India and potential legal implications.

A Step-by-Step Pre-Filing Checklist

Before filing your ITR, ensure you have all the necessary documents in order. Here’s a step-by-step checklist to help you:

- Gather all relevant documents, including salary slips, Form 16, and interest certificates.

- Verify your personal details, such as your name, date of birth, and PAN number.

- Check for any discrepancies in your salary slips and Form 16.

- Report all exempt income and foreign assets, if applicable.

- Ensure you have claimed the correct deductions under the old or new tax regime.

By following this checklist, you can identify potential errors and take corrective action to ensure a flawless filing.

Real-Life Example of a Common Filing Blunder

Example 1: Ignoring FD Interest Income

📖 Scenario:

Mr. Sharma had ₹10 lakh in fixed deposits.

He earned ₹70,000 interest but:

👉 Reported only salary income

👉 Ignored FD interest ❌

What Happened:

- Interest reflected in AIS

- Mismatch detected

- Received notice

Impact:

- Paid additional tax

- Interest under Sections 234B & 234C

Example 2: Wrong Capital Gains Classification

📖 Scenario:

Ms. Neha sold shares after 8 months

👉 Declared it as Long-Term Capital Gain ❌

What Happened:

- Actual classification: Short-Term

- Lower tax wrongly applied

Impact:

- Tax demand raised

- Interest + penalty

Example 3: Claiming Excess TDS

📖 Scenario:

Mr. Raj claimed ₹50,000 TDS

👉 But Form 26AS showed only ₹40,000

What Happened:

- System rejected excess claim

- Refund reduced

Impact:

- Delay in refund

- Tax demand raised

Example 4: Not Verifying ITR

📖 Scenario:

Mr. Verma filed ITR on time

👉 Forgot to verify return ❌

What Happened:

- Return treated as invalid

Impact:

- Missed deadline

- Had to file again with penalty

Example 5: Ignoring Gift Tax Rules

📖 Scenario:

Ms. Priya received ₹1.5 lakh gift from a friend

👉 Did not report it ❌

What Happened:

- Exceeds ₹50,000 limit

- Taxable under “Income from Other Sources”

Impact:

- Notice received

- Tax + penalty

Example 6: High-Value Transaction Not Explained

📖 Scenario:

Mr. X deposited ₹15 lakh cash

👉 Did not report corresponding income ❌

What Happened:

- AIS flagged transaction

- Notice issued

Impact:

- Asked to explain source

- Risk of penalty

Pro Tips for Streamlining Your Tax Season

To make your tax filing process smoother, consider the following pro tips:

- E-file your ITR: E-filing is faster and more convenient than traditional paper filing.

- Use tax filing software: Tax filing software can help you identify potential errors and ensure compliance.

- Keep records organised: Maintain a record of all your tax-related documents for easy access.

- Seek professional help: If you’re unsure about any aspect of your ITR, consider consulting a tax professional.

- Check AIS & Form 26AS

- ✔ Choose correct ITR form

- ✔ Report all income

- ✔ Verify deductions

- ✔ Check capital gains

- ✔ Validate TDS credits

- ✔ E-verify return within 30 days

- File early — avoid last-minute errors

- Cross-check with last year return

By following these tips and being meticulous during the filing process, you can avoid an income tax notice and ensure a stress-free tax season.

Conclusion

Accurate and compliant tax filing is crucial to avoid penalties and notices from the tax authorities. By understanding the common pitfalls and taking steps to ensure a smooth filing process, taxpayers can navigate the complexities of income tax return filing with confidence.

To ensure a hassle-free experience, taxpayers should refer to a comprehensive ITR filing checklist, verifying the accuracy of their personal details, income reporting, and deductions claimed. This proactive approach will help mitigate the risk of errors and subsequent repercussions.

Filing your Income Tax Return is not just a yearly formality — it is a reflection of your financial discipline and compliance.

In 2026, with advanced systems like AIS, data analytics, and automated scrutiny, the Income Tax Department already has access to most of your financial transactions.

👉 Your responsibility is to report it accurately, completely, and on time.

Key Takeaways

✔ Report all sources of income — even small or exempt ones

✔ Match your return with AIS and Form 26AS

✔ Avoid mistakes in capital gains, TDS, and deductions

✔ Disclose high-value transactions, gifts, and foreign assets properly

✔ Always verify your ITR after filing

💡 Final Thought

“In today’s transparent tax system, accuracy is not optional — it is essential.”

Closing Advice

👉 If you are unsure about any aspect of your return:

- Take professional guidance

- Or revise your return within time

👉 It is always better to correct a mistake voluntarily than to respond to a notice later.

By being informed and prepared, taxpayers can efficiently complete their tax filing obligations, avoiding last-minute rushes and potential mistakes. A well-prepared taxpayer is better equipped to handle the intricacies of tax filing, ensuring a seamless experience.

FAQ

What are the most common tax filing errors to look out for when submitting a return?

Some of the most common tax filing errors include providing incorrect bank account details, failing to report interest income from savings accounts, and mismatches between the income reported and the data in the Annual Information Statement (AIS). Taxpayers also frequently choose the wrong ITR form, which can lead to the return being declared defective.

How can I use an ITR filing checklist to ensure I don’t miss any critical steps?

A robust ITR filing checklist should include verifying your personal details, reconciling Form 26AS with your salary slips, ensuring all capital gains from platforms like Upstock are accounted for, and, most importantly, e-verifying your return after submission. Checking these off one by one helps prevent ITR filing mistakes in India that could lead to delays.

What steps should I take to avoid an income tax notice from the Department in 2026?

To avoid an income tax notice, always ensure that the income you declare perfectly aligns with the pre-filled data provided by the authorities. Be transparent about all sources of income, including freelance work on Freelancer.com or dividends, and make sure to pay any advance tax due before the end of the financial year to avoid interest penalties.

Are there specific income tax return mistakes in 2026 related to new digital assets?

Yes, income tax return mistakes 2026 often involve the incorrect reporting of Virtual Digital Assets (VDAs) like Bitcoin or Ethereum. Taxpayers must report these under the specific schedule for VDAs and pay the flat tax rate required; failing to disclose these transactions, even if they resulted in a loss, is a major compliance oversight.

Why is it so easy to make itr filing mistakes india regarding the new vs. old tax regimes?

The primary reason for ITR filing mistakes in India in this area is the complexity of deduction eligibility. Many taxpayers accidentally claim deductions such as HRA or Section 80C when opting into the New Tax Regime, which does not permit these exemptions. This leads to an immediate recalculation by the tax department and a subsequent tax demand.