“Bahut log mehnat karke paisa kamate hain…

lekin ek badi galti kar dete hain — paisa sahi jagah par allocate nahi karte.”

“Income badhane se zyada important hai — income ko sahi jagah lagana.”

Financial security depends heavily on where assets reside rather than just how much is earned. As we approach 2026 in personal finance, understanding your current habits becomes essential for long-term stability.

Most people keep their funds stagnant, missing out on growth opportunities. By reviewing your habits, you can identify whether your wealth works as hard as it should. This process helps ensure that every rupee serves a specific purpose, providing both safety and better returns.

Optimising your financial structure allows for greater peace of mind. When capital is placed correctly, it creates a robust foundation for future goals. Taking control today transforms your economic outlook for years to come.

Aap saving to kar rahe hain…

lekin ek important sawal hai:

👉 Kya aapka paisa sahi jagah rakha hai?

Sach yeh hai ki 90% log saving karte hain, lekin galat jagah par.

Result?

- Returns kam

- Risk zyada

- Aur financial stress

👉 Is blog mein hum ek simple aur practical tareeke se samjhenge ki money buckets kya hote hain, galtiyan kya hoti hain aur 2026 mein sahi allocation kaise karein.

Key Takeaways

- Organise your capital to ensure long-term financial stability.

- Review current habits to optimise wealth growth potential.

- Prioritise the correct placement of assets for better returns.

- Understand that structure determines your overall economic security.

- Adopt a proactive approach to manage your wealth effectively.

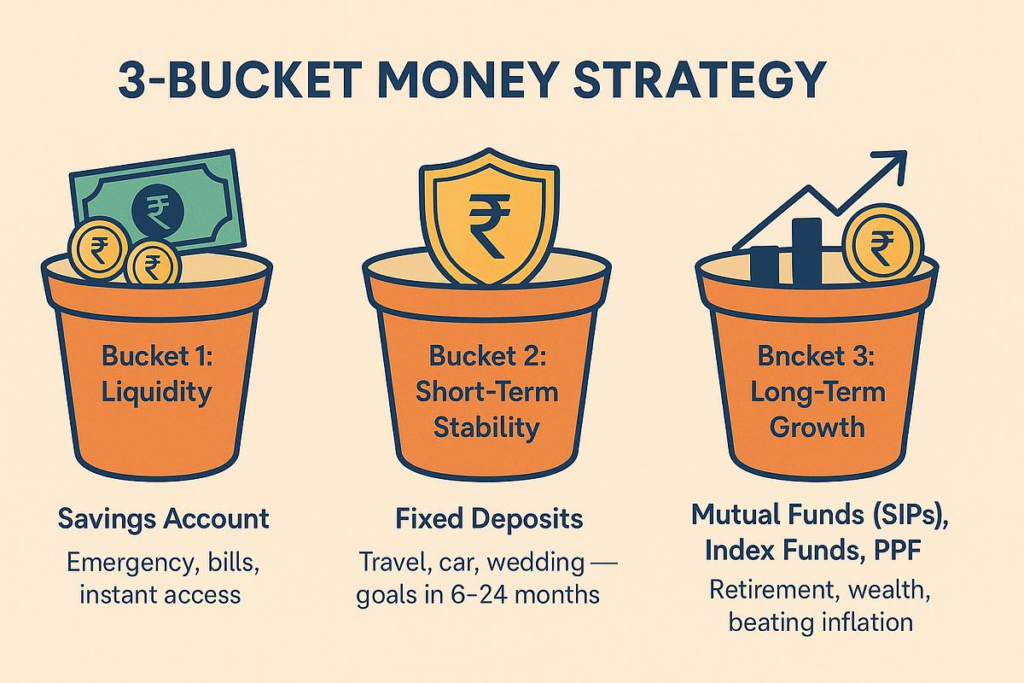

Understanding the Concept of Money Buckets

A bucket system transforms the way individuals view their financial health and future goals. By dividing savings into distinct parts, one can gain better control over one’s economic life. Mastering these investment basics allows anyone to build a resilient portfolio that withstands market shifts.

Money buckets ka matlab hai:

👉 Apne paiso ko unke purpose ke hisaab se divide karna

Jaise ghar mein har cheez ka alag dabba hota hai, waise hi har paisa ka ek role hota hai.

Defining the Bucket System for Personal Finance

The bucket strategy involves allocating capital across three categories based on time horizons. The immediate bucket Safety. This ensures that essential costs are covered without needing to sell long-term assets during a market downturn.

The intermediate bucket focuses on goals for the next few years, such as stability, buying a vehicle, or planning a holiday. Finally, the long-term bucket is reserved for wealth creation, retirement planning or children’s education. These investment basics provide a clear roadmap for every rupee earned.

| Bucket Type | Primary Purpose | Asset Class |

|---|---|---|

| Safety | Daily Expenses | Savings Accounts |

| Stability | Mid-term Goals | Debt Funds |

| Growth | Wealth Creation | Equity Markets |

🟢 1. Safety Bucket (Emergency Money)

Yeh paisa aapki security hai.

Includes:

- Savings account

- Liquid mutual funds

Use:

- Medical emergency

- Job loss

- Urgent expenses

👉 Rule: Easy access + zero risk focus

👉 Anchor:

Agar aapne abhi tak emergency fund banane ka sahi tareeka nahi samjha hai, to pehle yeh guide zaroor padhein. Emergency Fund in 2026

🟡 2. Stability Bucket (Medium-Term Money)

Yeh paisa planned goals ke liye hota hai.

Includes:

- Fixed Deposits

- Debt Mutual Funds

Use:

- Car purchase

- Education

- 1–5 saal ke goals

👉 Rule: Stable return + low volatility

👉 Anchor:

“FD vs Debt Mutual Fund ka comparison”Fixed Deposit vs Debt Mutual Funds in 2026: Which Is Better?

🔴 3. Growth Bucket (Wealth Creation Money)

Yeh paisa long-term growth ke liye hota hai.

Includes:

- Equity Mutual Funds

- Stocks

Use:

- Retirement

- Wealth creation

👉 Rule: High return + patience

👉 Anchor:

“Stock Market Investment Basics” Stock Market in 2026:

Why Categorisation Prevents Financial Leakage

Financial leakage often occurs when money lacks a specific purpose or destination. When funds are lumped together, it becomes easy to spend savings meant for the future on impulsive current desires. Categorisation forces a disciplined approach, ensuring that every pound or rupee has a clear job to perform.

By assigning each bucket a unique role, individuals avoid the trap of using long-term capital for short-term needs. This structured approach protects the integrity of one’s financial plan. It creates a barrier against unnecessary spending and keeps the investor focused on their ultimate objectives.

📊 Ideal Money Allocation Model :-

| Category | Suggested % |

|---|---|

| Expenses | 50% |

| Investments | 25–30% |

| Emergency Fund | 10–15% |

| Insurance | 5–10% |

| Lifestyle | Balance |

Saving is Not Enough: Why Placement Matters More

While saving is the foundation of personal finance, the way you allocate those funds determines your long-term success. Many individuals focus solely on saving money, yet they overlook the importance of investment basics. Simply accumulating cash in a standard account is often insufficient to keep up with the rising cost of living in India.

🔹 PRACTICAL EXAMPLE

Mr. B earns ₹1,00,000 per month:

- ₹50,000 → Expenses

- ₹25,000 → Investments

- ₹10,000 → Emergency fund

- ₹5,000 → Insurance

- ₹10,000 → Lifestyle

👉 Result:

- Financial stability

- Future security

- Stress reduction

👉 Common Money Allocation Mistakes in 2026

(Avoid These Errors)”

❌ Saara paisa ek jagah rakhna

Bank mein → low return

Stocks mein → high risk

❌ Emergency fund ignore karna

👉 Result: Investment todni padti hai

❌ Goals mix karna

Retirement + short-term goals same jagah

❌ Time horizon ignore karna

Short-term paisa equity mein dal dena

❌ Review na karna

Income badh rahi hai… par allocation wahi hai

The Inflation Trap in Traditional Savings Accounts

Inflation acts as a silent thief, gradually eroding the real value of your hard-earned money. When your capital sits in a traditional savings account, the interest earned often fails to keep pace with the annual rate of inflation. This means that while the number in your bank statement might increase, your actual purchasing power is steadily declining.

“Wealth is not just about how much you save, but how effectively you put that money to work for your future.”

If your money remains stagnant, you are effectively losing value every single year. Relying on low-interest vehicles for long-term goals is a common mistake that prevents many from achieving true financial freedom.

👉 Anchor:

“inflation ka impact wealth par kaise padta hai”Inflation Quietly Destroys Your Wealth (2026 Guide)

The Difference Between Idle Cash and Strategic Capital

There is a fundamental distinction between keeping money idle and deploying it as strategic capital. Idle cash is money that sits in a low-yield environment, waiting for a purpose that may never arrive. In contrast, strategic capital is positioned to grow through various financial instruments, ensuring your wealth works as hard as you do.

By mastering investment basics, you can shift your mindset from mere accumulation to active wealth management. This transition is essential for anyone looking to maintain their lifestyle and reach their goals in the coming years. Moving your funds into the right buckets ensures they are positioned for growth rather than stagnation.

Even the most diligent savers often stumble when managing their asset allocation. When investors fail to align their holdings with specific time horizons, they often make financial mistakes that hinder long-term growth. Recognising these errors is the first step toward building a more resilient financial future.

👉 Anchor:

Asset Allocation

Smart Asset Allocation Strategy for Stable & Growing Income

Over-Reliance on Low-Yield Instruments

Many individuals feel safest keeping the bulk of their capital in traditional savings accounts or fixed deposits. While these provide a sense of security, they often fail to keep pace with inflation over the long term. Relying too heavily on these low-yield options is one of the most common asset allocation mistakes that erodes purchasing power.

Ignoring the Impact of Taxation on Returns

Investors often focus solely on the headline interest rate without considering the tax implications. In India, interest earned on certain instruments is fully taxable at the investor’s slab rate, which significantly reduces the net return. Failing to account for these tax outflows is a classic error that can leave a portfolio underperforming its potential.

The Danger of Mixing Emergency Funds with Long-Term Investments

A critical error involves blending short-term liquidity needs with long-term wealth creation goals. When emergency funds are tied up in volatile market instruments, an unexpected life event may force an investor to sell assets during a market downturn. This forced selling locks in losses and disrupts compounding.

To maintain a healthy trajectory, it is essential to rebalance buckets regularly. This practice ensures that each category is properly funded and aligned with its intended purpose. By keeping these funds separate, investors protect their long-term strategy from the unpredictable nature of daily life.

A Quick Self-Check for Your Current Portfolio

Financial clarity begins with a simple, honest assessment of where your capital resides today. Many investors overlook the importance of periodic reviews, which often leads to common asset allocation mistakes that hinder long-term growth. By taking a proactive approach, one can ensure that every rupee is positioned to serve a specific purpose.

Khud se yeh sawal poochiye:

- Kya mere paas 6 months ka emergency fund hai?

- Kya mera short-term aur long-term paisa alag hai?

- Kya main ek hi jagah invest nahi kar raha?

- Kya main panic nahi karta market girne par?

- Kya main yearly review karta hoon?

📌 Interpretation:

- 0–2 YES → High risk situation

- 3–4 YES → Moderate balance

- 5–6 YES → Strong financial discipline

👉 Agar inme se aadhe sawalon ka jawab “NO” hai, to correction zaroori hai

Assessing Your Liquidity Ratios

Liquidity ratios serve as a vital health check for your personal finances. They help determine if you have enough accessible cash to cover your immediate obligations without needing to liquidate long-term investments prematurely. If your ratio is too low, you might find yourself forced to sell assets during a market downturn.

To calculate this, simply divide your liquid assets by your monthly expenses. A healthy buffer ensures that you remain financially resilient even when unexpected costs arise. Maintaining this balance prevents the need to dip into retirement funds or high-growth portfolios for daily living expenses.

Identifying Mismatched Time Horizons

A common error occurs when investors place short-term goals into long-term vehicles, or vice versa. For instance, keeping money meant for a house deposit in a volatile equity fund can be risky if the market drops right before you need the cash. Conversely, leaving long-term wealth in a low-interest savings account often results in a loss of purchasing power due to inflation.

Reviewing your portfolio helps you spot these mismatched time horizons before they become significant problems. Ensure that your investment duration aligns perfectly with your financial objectives. This simple alignment is the most effective way to avoid unnecessary asset allocation mistakes and keep your wealth-building journey on the right track.

The Correct Bucket Strategy for Indian Investors

A well-planned savings strategy in India acts as a roadmap for your financial journey. By dividing your capital into specific buckets, you ensure that your money works as hard as you do while remaining accessible when life takes an unexpected turn.

🧠 “Divide before you invest”

Step 1: Identify time horizon

| Time | Bucket |

|---|---|

| 0–1 year | Safety |

| 1–5 years | Stability |

| 5+ years | Growth |

Step 2: Allocate percentage

👉 Simple model:

- Safety: 10–20%

- Stability: 30–40%

- Growth: 40–60%

Step 3: Automate flow

👉 Salary aate hi:

- Emergency fund first

- SIP second

- Spending last

📌 Rule: “Pay yourself first”

The Short-Term Bucket: Liquidity and Safety

The primary goal of this bucket is to provide immediate access to cash. It should hold at least three years’ worth of your essential expenses to protect your lifestyle during market downturns or personal emergencies.

Investors often prefer high-yield savings accounts, liquid mutual funds, or sweep-in fixed deposits for this purpose. Keeping these funds separate ensures that you never have to sell long-term assets at a loss when you need cash quickly.

The Medium-Term Bucket: Balancing Growth and Stability

Once your safety net is secure, the medium-term bucket focuses on goals that are three to seven years away. This might include planning for a child’s education or a down payment on a home.

You should aim for a mix of debt and equity instruments here. Balanced advantage funds or conservative hybrid funds are excellent choices for this phase, as they offer a buffer against volatility while still providing better returns than traditional bank deposits.

The Long-Term Bucket: Wealth Creation and Compounding

The long-term bucket is your engine for wealth creation, designed for goals more than 7 years away, such as retirement. Because you have time on your side, you can afford to be more aggressive with your asset selection.

Equity mutual funds, direct stocks, and diversified portfolios are ideal for this category. By maintaining a disciplined savings strategy in India, you allow compounding to multiply your wealth significantly over several decades. Regular monitoring of these investments ensures that your portfolio remains aligned with your evolving financial aspirations.

Real-Life Example: Applying the Strategy

Consider the journey of Johny and Reema as they navigate their financial future in 2026. Like many working professionals, they initially kept all their funds in a single, low-interest savings account. They soon realised that this passive approach hindered their long-term growth potential.

By adopting a structured bucket system, they transformed their financial outlook. This method allowed them to categorise their capital based on specific time horizons and liquidity needs. It provided them with the peace of mind that every rupee was working towards a defined goal.

👉

“This simple bucket strategy is widely used by financial planners to manage risk and optimise returns.”

Scenario Analysis: The Working Professional in 2026

Johny and Reema decided to divide their total investable surplus of Rs300,000 into three distinct buckets. This strategic move ensured that their immediate needs were met while their long-term wealth continued to compound effectively.

The following table illustrates how they distributed their capital to balance safety, growth, and stability:

| Bucket Type | Allocation Amount | Primary Objective |

|---|---|---|

| Immediate | Rs50,000 | Liquidity and Safety |

| Intermediate | Rs100,000 | Growth and Stability |

| Long-Term | Rs150,000 | Wealth Creation |

This clear division helped them avoid the common trap of keeping too much cash idle. By assigning a purpose to each portion of their wealth, they reduced the risk of impulsive spending or poor investment choices.

Visualising the Shift from Savings to Strategic Allocation

Moving from a single savings account to a multi-bucket strategy requires a shift in mindset. It is no longer about how much you save, but where you place your capital to maximise returns. Johny and Reema found that this transition offered several key advantages:

- Enhanced Clarity: They could easily track progress toward specific life milestones.

- Reduced Anxiety: Knowing their emergency funds were secure allowed them to take calculated risks elsewhere.

- Optimised Returns: Each bucket was invested in instruments that matched its specific time horizon.

This practical example demonstrates that effective planning is the cornerstone of financial security. By following this model, you can demystify the wealth management process. Taking control of your finances today creates a much clearer path for your future success.

👉 “Smart Money Allocation Strategy for 2026 (Step-by-Step)”:

Navigating Market Trends

As the year 2026 unfolds, investors must refine their strategies to keep pace with shifting market dynamics. Achieving long-term stability in personal finance in 2026 requires a proactive approach rather than a reactive one. By staying informed, individuals can ensure their capital remains productive even when economic conditions fluctuate.

- “Agar aap apni investments ko balance karna chahte hain, toh yeh guide zaroor padhein:

👉 How to Rebalance Your Portfolio in 2026”Step-by-Step Practical Guide

🟢 Strategy 1: Salary-Based Allocation

- Salary aate hi fixed rule follow:

- 20% investment

- 10% emergency buffer

- rest expenses

🟢 Strategy 2: Step-Up Investment

👉 Har saal SIP increase:

- Salary increase → SIP increase 10–15%

🟢 Strategy 3: Rebalancing Rule

👉 Every 6–12 months:

- Equity too high → shift to debt

- Debt too high → increase equity

🟢 Strategy 4: Goal Mapping

👉 Har investment ka goal fix:

- Emergency → Safety bucket

- Car/home → Stability

- Retirement → Growth

🟢 Strategy 5: Emotional Control Rule

👉 Market crash = buying opportunity

👉 Market boom = discipline

📌 Rule: “Emotion ko portfolio se alag rakho”

Adapting to Changing Interest Rate Environments

Interest rates act as the heartbeat of any financial plan. When rates shift, the performance of short-term cash buckets often changes, requiring immediate attention to maintain real returns. Flexibility is the key to ensuring that your liquid assets do not lose value against rising costs.

“The secret to wealth is not just in what you earn, but in how you adapt your strategy to the changing tides of the economy.”

To stay ahead, consider these steps for your cash management:

- Review your savings accounts every quarter to ensure they offer competitive yields.

- Shift excess idle cash into higher-yielding instruments if interest rates remain elevated.

- Maintain a clear distinction between emergency funds and growth-oriented capital.

Incorporating Digital Assets and Modern Financial Instruments

The landscape of personal finance 2026 is increasingly influenced by digital innovation. Modern investors are now looking beyond traditional bank deposits to diversify their portfolios effectively. Integrating digital assets can provide a hedge against traditional market volatility when managed with caution.

It is essential to approach these new instruments with a disciplined mindset. While technology offers exciting opportunities for growth, it should never replace the foundational safety of your core financial buckets. Always prioritise security and regulatory compliance when exploring modern investment avenues to protect your hard-earned wealth.

Mistakes to Avoid and the Way Forward

Navigating the financial landscape requires a keen eye for potential traps that could derail your progress. Many individuals find themselves in difficult positions simply because they fail to recognise the early warning signs of poor planning. By staying alert, you can avoid common money mistakes that often hinder long-term wealth accumulation.

Common Pitfalls to Watch Out For in the Coming Year

One frequent error is the tendency to chase short-term market trends without considering the underlying fundamentals. Investors often feel the pressure to jump into the latest “hot” asset, only to realise later that it does not align with their personal risk profile. This impulsive behaviour frequently leads to unnecessary losses and unwanted stress.

Another significant issue is the failure to account for inflation’s eroding power on idle cash. Keeping too much money in low-interest savings accounts might feel safe, but it effectively reduces your purchasing power over time. Furthermore, neglecting to diversify across different asset classes leaves your portfolio vulnerable to sector-specific downturns.

Building a Sustainable Financial Roadmap

A truly robust financial plan is not a static document; it is a living strategy that evolves with your life circumstances. Sustainable financial roadmaps require regular monitoring and rebalancing to keep your buckets aligned with your goals. This process ensures that your capital remains productive regardless of shifting economic conditions.

To move forward effectively, you should schedule quarterly reviews to assess your progress. During these sessions, check if your asset allocation still matches your time horizons and risk tolerance. If a particular bucket has grown significantly, consider reallocating the excess to maintain your intended balance.

Ultimately, the way forward is to make consistent, informed decisions rather than reacting to market noise. By documenting your strategy and sticking to your plan, you protect yourself from the emotional traps that lead to costly money mistakes. Taking control today is the most reliable path to achieving your long-term financial aspirations.

👉

“Aap apni current savings ko ek baar review karke dekhiye — kya aapka paisa sahi buckets mein hai?”

👉 Anchor:

“portfolio rebalance kaise karein (next blog)”

Agar aapka allocation already bigad chuka hai, to next step hai portfolio ko rebalance karna – jiska detailed guide hum next blog mein cover karenge.”

Conclusion:-

Effective wealth management relies on where you place your money, not just on saving. A robust savings strategy in India helps individuals organise their capital into distinct buckets for immediate needs, medium-term goals, and long-term growth. This structured approach ensures that liquidity remains available while your investments work hard to beat inflation.

Many people often ask if they should rebalance their portfolios frequently. Experts suggest reviewing your asset allocation at least once a year to ensure it aligns with your changing life stages. Another common query involves choosing the right instruments for each bucket. It is wise to stick with reliable options, such as liquid funds for short-term needs and diversified equity mutual funds for long-term wealth creation.

Adopting this disciplined savings strategy, India transforms how you view your bank balance. It turns idle cash into a powerful tool for your family’s future prosperity. Start categorising your assets today to build a resilient financial roadmap that stands the test of time.

Saving karna achhi baat hai…

lekin sahi jagah saving karna sabse important hai.

👉 Wealth creation ka secret earning mein nahi, allocation mein chhupa hai.

FAQ:-

What are the core investment basics of the three-bucket system?

The bucket system is a method of organising personal wealth into three distinct categories based on time horizons: immediate, intermediate, and long-term. By following these investment basics, an individual ensures that every pound or rupee is assigned a specific task, such as covering monthly bills or funding a retirement decades away. This structured approach is essential for preventing financial leakage and maintaining a disciplined savings strategy in India and other global markets.

Why is simply saving cash considered a risk for personal finance 2026?

While keeping money in a standard account at HSBC or the State Bank of India feels safe, inflation acts as a silent tax that erodes purchasing power. In the context of personal finance 2026, merely accumulating “idle cash” is often insufficient. To combat the rising cost of living, wealth must be moved into “strategic capital”—investments that have the potential to outpace inflation and grow in real value over time.

What are the most common asset allocation mistakes to watch out for?

One of the most frequent asset allocation mistakes is failing to align investments with a specific timeframe. This often includes an over-reliance on low-yield instruments, like traditional fixed deposits, which may not meet long-term goals after tax. Additionally, many people make the error of mixing their emergency fund with their long-term growth capital, leading to the forced sale of assets during a market downturn, which can permanently damage a portfolio’s trajectory.

How can a professional implement a successful savings strategy in India?

A robust savings strategy in India requires utilising the three-bucket model tailored to local instruments. The short-term bucket should focus on liquidity and safety, perhaps using liquid funds from ICICI Prudential. The medium-term bucket balances growth and stability, while the long-term bucket acts as a wealth engine, often utilising diversified equity funds like the UTI Nifty 50 Index Fund to harness the power of compounding over several decades.

Which money mistakes are most likely to derail a financial plan in 2026?

Looking ahead, common money mistakes include failing to adapt to a changing interest rate environment and ignoring the impact of taxation on net returns. Many investors also neglect to diversify into modern financial instruments or digital assets, which can leave a portfolio stagnant. By failing to conduct regular “self-checks” on liquidity ratios and time horizons, an investor risks being caught off-guard by shifting market trends in the coming year.

How does a real-life professional like Vikram, an engineer at Tata Consultancy Services, apply this strategy?

In a practical 2026 scenario, a professional like Vikram or Ananya would use Zerodha to segment their capital. They might keep six months of expenses in a high-interest savings account for immediate needs, allocate medium-term funds to a balanced advantage fund, and direct their long-term capital into a diversified equity portfolio. This shift from passive saving to active, strategic allocation ensures that their wealth works as hard as they do, providing both security and growth.

Kitna % invest karna chahiye?

👉 Ideally 20–30% income invest karna chahiye

Emergency fund kitna hona chahiye?

👉 6–12 months expenses

Sabse common mistake kya hai?

👉 Pehle kharch, baad mein saving (ulta hona chahiye)

👉 Last Updated on: 1 May 2026

Disclaimer

This publication is intended solely for informational and educational purposes and does not constitute professional, legal, tax, or financial advice. The information provided has been compiled from sources believed to be reliable; however, its accuracy, completeness, or current relevance is not guaranteed. The views and opinions expressed herein reflect the author’s understanding at the time of publication and are subject to change without notice.

Readers are strongly advised to seek independent professional advice before making any decision or taking any action based on the information contained in this publication. The author and publisher expressly disclaim any responsibility or liability for any loss, damage, or consequence arising directly or indirectly from reliance on this content or from any action taken or not taken based on it.