Relying on a single salary has become riskier in today’s volatile economy. Job roles change, health shocks happen and markets can shift quickly; true stability now comes from managing money across different sources rather than depending on one employer.

Aaj ke time mein sirf ek income source par depend rehna financial risk ban chuka hai.

Job kabhi bhi ja sakti hai, business slow ho sakta hai, health issue aa sakta hai — aur income ruk sakti hai.

👉 Isliye smart log 2026 mein ek hi rule follow kar rahe hain:

“Never depend on a single income — create multiple income streams.”

Agar aap sote waqt bhi paisa kama rahe hain, tabhi aap truly financially secure hain.

Many people are taking a proactive approach to long-term prosperity. By diversifying income streams — for example, combining salary, investment returns and a small digital product — they reduce exposure to sudden downturns and build steady money growth over time.

Developing passive income is central to this approach: once set up, these streams can generate revenue with much less ongoing time input. This guide sets out practical, step-by-step 2026 finance tips to help anyone move from a single paycheque to a balanced portfolio of income sources.

Key Takeaways

- Diversification reduces the risk of relying on a single income source.

- Relying on one salary creates vulnerability during market or job shifts.

- Passive earnings can provide a reliable buffer for unexpected life events.

- Strategic planning and simple products (courses, digital content) speed progress toward long-term goals.

- Adopt a stepwise mindset: build accounts, protect cash, then scale revenue streams.

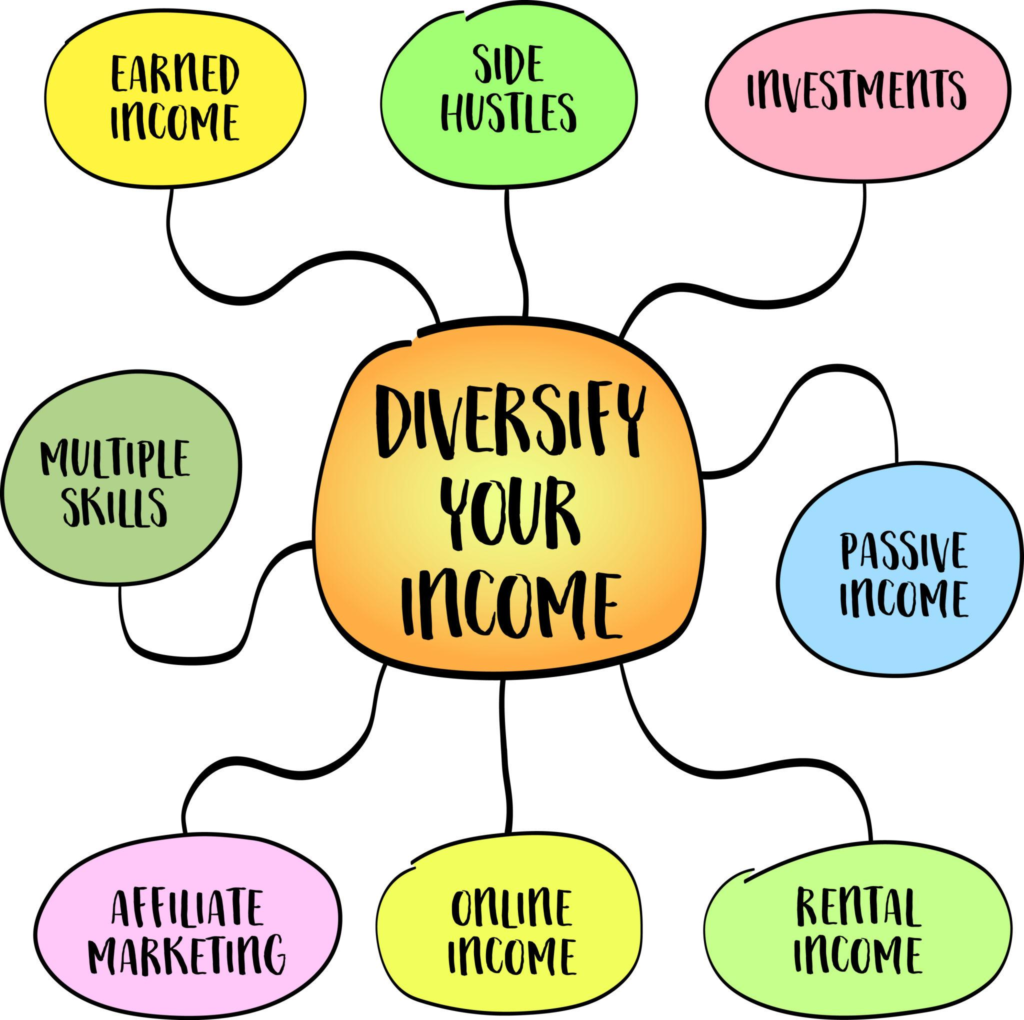

Understanding the Concept of Multiple Income Streams

Developing multiple income streams is a practical way to create a more resilient financial base. Rather than depending solely on a salary, people combine different sources of income so that a setback in one area does not stop all cash flow.

👉 Alag-alag sources se income aana

Example:

- Salary / Business income

- Rental income

- Interest / Dividend

- Blogging / Online income

👉 Simple samajhiye:

Ek pipe se paani aa raha hai vs 4 pipe se paani aa raha hai

Inflation silently reduces your purchasing power, which is why understanding the impact of inflation on your wealth is extremely important. Inflation Quietly Destroys Your Wealth (2026 Guide)

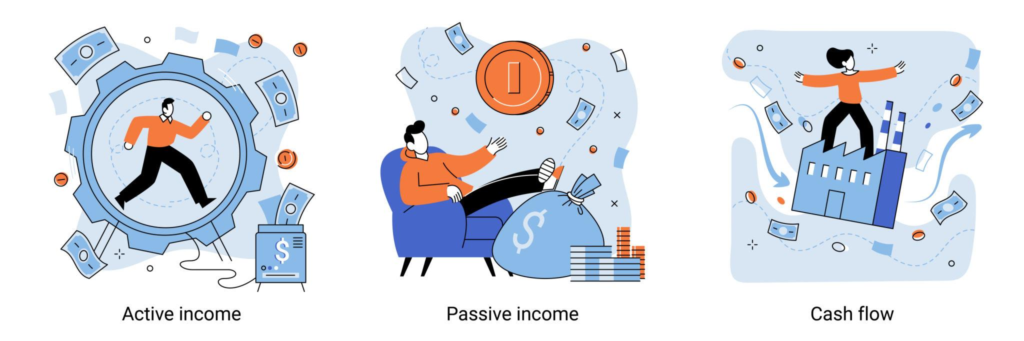

Defining Active versus Passive Income

Active income is the familiar model: trading time for money. Examples include a monthly salary, freelancing paid by the hour, or contract work. The main limitation of active income is time — earnings usually stop when work stops.

Passive income, by contrast, is income that continues with minimal daily effort once set up. Examples include a well-priced digital course, a small niche website that earns ad revenue, or dividend payments from investments. Passive streams normally require an initial period of higher effort, then lower maintenance over time.

How to generate passive Income How to Generate Passive Income in 2026

Quick examples to illustrate the difference:

- Active: a copywriter charging per article and invoicing clients weekly.

- Passive: an online course that continues to sell while the creator works on other projects.

The Philosophy of Wealth Accumulation

At its core, the shift is from being a wage earner to becoming an asset builder. It is less about earning more in the short term and more about using existing income to buy or build assets that generate future returns. That might mean saving part of a salary to invest in funds, creating a digital product, or starting a small side business.

People who prioritise multiple streams can decouple lifestyle from a single job and create steady, long-term growth. Micro-action: list current earnings by type — salary, freelance, investment, and any small products — to see where to start building a new stream.

Why Diversification is Essential for Financial Stability in 2026

Financial security in 2026 requires more than a steady job; it needs a deliberate plan for where income comes from. Relying on a single paycheque creates a single point of failure if a business slows or a role is cut. Income diversification is the simplest practical way to make personal finances more resilient.

- 🔸 Job uncertainty (AI & automation impact)

- 🔸 Inflation continuously badh raha hai

- 🔸 Expenses fast increase ho rahe hain

- 🔸 Financial independence ka goal

👉 Example:

- Sirf salary ₹50,000 → risk high

- 4 income sources ₹12,500 each → safe + stable

Mitigating Economic Volatility

The global market changes frequently, so having multiple income streams that do not move together creates a natural safety net. Spreading money across wages, investments and passive sources reduces the effect of any one market shock and makes overall cash flow steadier.

- Less correlation: different streams often react differently to the same shock.

- Smaller drawdowns: a fall in one area is cushioned by others.

- Improved peace of mind: fewer sleepless nights when one source dips.

Example: a software engineer who keeps a core salary, earns freelance fees from short projects and receives dividend payments from investments will be better able to handle a lay-off than someone dependent only on salary.

Protecting Against Career Redundancy

Career paths are more fluid than before; roles can change or disappear. Secondary income streams provide the financial breathing room needed to retrain, search for a new role or scale a side project. Developing marketable skills outside a primary job — for instance freelance consulting or a digital product — acts as a practical insurance policy.

Micro-action: identify two skills you could monetise this year and one small investment you could start to build passive income.

Core Framework for Categorising Income Streams

To build multiple income streams effectively, it helps to sort every source of income into clear buckets. Organising where money comes from makes decisions simpler and highlights which areas need more attention or investment.

This practical framework uses three primary buckets: earned, portfolio and passive income. Each plays a different role on the path to financial independence and should be built in sequence.

Earned Income from Primary Employment

Earned income is the steady foundation: the salary or wages that pay the bills and fund savings. It usually requires the least financial risk but the most time and ongoing work.

Example and expectation: a full‑time salary — high ongoing time commitment, immediate cash flow, low setup cost. Use earned income first to build an emergency account and seed initial investments.

Active Income

- Job

- Freelancing

- Consulting

👉 Time ke badle paisa

Semi-Passive Income

- Blogging

- YouTube

- Online courses

- Affiliate marketing

👉 Initial mehnat, baad mein income flow

Passive Income

- Mutual Funds (SIP/SWP)

- Dividend stocks

- Rental income

- Bonds / FD

👉 Money works for you

Portfolio Income from Investments

Portfolio income comes from capital invested in markets: mutual funds, equity stocks and bonds. This income grows over time through returns and compounding and requires some initial capital and ongoing monitoring.

Example and expectation: a monthly SIP into mutual funds — low monthly time, gradual growth over years, moderate risk. Portfolio investments make your money work while you focus on other streams.

Passive Income from Digital Assets

Passive income is typically generated by assets that need a greater upfront effort but less maintenance later. Common sources include online courses, e‑books, niche websites or small digital products that sell repeatedly.

Example and expectation: creating an online course — high initial effort (content, production), 6–12+ months to gain traction, low ongoing time once automated. These streams are highly scalable and can become a major part of long‑term income.

Quick comparison:

- Earned: immediate cash, high time, low setup — e.g. salary.

- Portfolio: compounding returns, low weekly time, medium setup — e.g. SIPs or stocks.

- Passive: scalable products, high initial effort, low maintenance — e.g. digital course.

How to start: first build a 3–6 month emergency account from earned income, then allocate small monthly amounts into investment funds and begin one passive product or content project. Micro‑action: map your current earnings into these three buckets and pick one small step for each.

How to Build Multiple Income Streams in 2026 (Practical Guide for Financial Freedom)

Achieving practical financial freedom in 2026 begins with a clear, step‑by‑step plan. Many people feel overwhelmed by the idea of managing several income sources, but a systematic approach turns the task into manageable stages. This section breaks the process down into simple actions anyone can follow.

Best Income Streams to Start in 2026

📌 Digital Income

- Blogging

- Affiliate marketing

- E-books / courses

📌 Financial Income

- Mutual Funds SIP

- Dividend Stocks

- REITs

📌 Skill-Based Income

- GST & Income Tax consultancy

- Freelancing

📌 Asset-Based Income

- Rental property

- Small commercial assets

Step-by-Step Strategy to Build Multiple Income Streams

Once you start earning from multiple sources, proper monthly investment planning becomes essential to grow your wealth consistently. How Much Should You Invest Every Month in 2026?

Once you start earning from multiple sources, proper monthly investment planning becomes essential to

✅ Step 1: Stabilize Primary Income

Sabse pehle apni main income stable rakhiye

✅ Step 2: Start One Side Income

👉 Example: Blogging (FinanceKiBaatein.com)

✅ Step 3: Reinvest Income

Blog income → Mutual funds / stocks

✅ Step 4: Add 2nd & 3rd Income

- Consultancy

- Affiliate income

✅ Step 5: Automate Income

- SIP

- SWP

- Digital products

🟦 Practical Example (Real-Life Scenario)

Manoj ki monthly income:

- Salary → ₹50,000

- Blog → ₹10,000

- SIP returns → ₹5,000

- Freelancing → ₹15,000

👉 Total Income = ₹80,000

👉 Risk bhi kam + growth bhi fast

1. Assess Current Financial Resources

Begin by reviewing current accounts, earnings and monthly outgoings. Build an emergency fund covering three to six months of essential expenses — adjust this range for family commitments or irregular income. This safety net lets people experiment with new income streams without risking day‑to‑day stability.

2. Identify Skill Gaps and Market Needs

Find where personal expertise meets demand. In the Indian market this might include digital services, local consulting or niche content. Make a short list of ten marketable skills and five product or service ideas that match those skills.

3. Allocate Time for Side Ventures

Time is limited, so protect it. Treat side projects like a professional task: block specific hours each week and set small, measurable goals. Practical tips:

- Audit one week to find two to five hours of repeatable time slots.

- Prioritise tasks that move revenue forward — product creation, marketing, client outreach.

- Use automation tools (email autoresponders, scheduling apps) to save time.

4. Start Small and Scale

Launch low‑cost experiments: a short online course, a niche blog, or a freelance offering. Track results for 12 weeks. If a project gains traction, reinvest some profits to scale — paid promotion, better tools, or outsourcing routine work. Case studies:

- Anna built a short course in six months that began covering her monthly subscription costs within a year.

- Mike used freelance projects to save a deposit; after 18 months he increased rates and replaced part of his salary.

Micro‑action for this week

Create an audit sheet: list all current income sources and accounts; note weekly time available; write down two skills to monetise and one product idea to test. Commit to a 12‑week experiment for the chosen idea.

Top Income Stream Opportunities for the Indian Market

The modern Indian economy offers a range of practical ways to earn beyond a standard salary. Focusing on sensible income diversification helps people build a more resilient financial base. Below are four accessible options — from low‑cost digital products to traditional property — with quick suitability notes and simple steps to begin.

Before building multiple income streams, it is important to have a strong emergency fund strategy to handle unexpected financial situations.Where to Stash Your Emergency Fund in 2026

Leveraging Freelance Platforms for Global Clients

Quick suitability: low capital, high time; good for people with in‑demand skills.

Freelancing on platforms such as Upwork and Fiverr is one of the fastest ways to start earning extra money. Services in demand include graphic design, coding, content writing and digital marketing. Global clients typically pay in stronger currencies, which can boost local purchasing power.

How to start:

- Create a clear profile showcasing 3–5 best projects or samples.

- Set competitive rates, then raise them as you gain reviews.

- Use templates and tools to speed proposals and invoicing.

Example timeline: many freelancers win first paid gigs in 4–12 weeks with consistent outreach.

Investing in Indian Mutual Funds and Stocks

Quick suitability: low to medium capital, low weekly time; suits long‑term investors.

Systematic Investment Plans (SIPs) into mutual funds and selective equity investments offer portfolio income through compounding. These are a practical way to participate in the growth of the Indian economy without needing deep stock‑picking expertise.

How to start:

- Open an account on a regulated platform (Zerodha, Groww or similar) and set up a monthly SIP.

- Choose diversified equity or balanced funds to match risk tolerance.

- Review allocation annually and keep an emergency account separate.

Example timeline: SIPs typically show meaningful benefits over several years; aim for at least a 3–5 year horizon.

Monetising Content Creation and Digital Courses

Quick suitability: low capital, high initial effort; suits people with teachable expertise or creative content.

Creating digital products — online courses, niche blogs, paid newsletters or YouTube channels — turns knowledge into passive income. While the upfront work is significant, these digital products can scale without proportional increases in time.

How to start:

- Validate demand with a short free lead magnet or mini‑course.

- Record and launch a basic course using platforms such as Udemy, Teachable or self‑hosted options.

- Use basic marketing: email, SEO for a blog, YouTube snippets or affordable ads.

Example timeline: a course or niche site often needs 6–12 months to build steady sales; reinvest early earnings into marketing or product improvements.

Real Estate and Rental Yield Strategies

Quick suitability: high capital, moderate ongoing effort; suits people seeking long‑term stability and rental income.

Real estate can provide rental income and capital appreciation. It requires more initial capital and local market knowledge, but offers a different risk and return profile to digital or market investments.

How to start:

- Research local markets and rental yields; consider emerging urban hubs cautiously and check local vacancy and price trends.

- Explore REITs or fractional property platforms if a direct purchase is not affordable.

- Factor in taxes, maintenance and management costs when forecasting rental income.

Example timeline: property investments are generally medium- to long-term (years) for meaningful returns; fractional or REIT options can be quicker to start.

| Income Stream, Initial Capital, Effort Level, Risk Profile | |||

| Freelancing | Very Low | High | Low |

| Mutual Funds / Stocks | Low | Low | Moderate |

| Digital Courses / Content | Low | High | Low |

| Real Estate / REITs | High | Moderate | Moderate |

Decision checklist: pick one low‑capital option to test within 12 weeks (freelance gig or small digital product) and set up one monthly SIP into funds. Track time spent and revenue for each stream in separate accounts to see which to scale next.

A Practical Example of a Balanced Income Portfolio

A clear, well‑structured portfolio acts as a simple roadmap for someone aiming to escape the cycle of living paycheque to paycheque. Diversifying income sources helps move steadily towards practical financial freedom while managing downside risk.

The Profile of an Aspiring Financial Independent

Imagine a 32‑year‑old software engineer earning a steady salary who wants to build wealth beyond their job. They favour long‑term security over quick wins and have a moderate risk appetite, so they choose a mix of safe and growth assets and set clear milestones for each rupee invested.

Step‑by‑Step Implementation of the Strategy

1) Build liquidity: keep a 3–6 month emergency account in a high‑yield savings account or liquid mutual fund so cash is available for shocks without touching long‑term investments.

2) Add fixed income: allocate a portion to PPF, corporate bonds or fixed deposits to generate steady returns and reduce portfolio volatility.

3) Grow with equities: dedicate a portion to equity mutual funds or select stocks for inflation‑beating growth over years.

Sample allocation for this profile (example):

| Bucket Example allocation | |

| Liquidity / Emergency | 30% |

| Fixed income / Debt funds | 30% |

| Equity / Growth funds & stocks | 30% |

| Passive projects (course, blog, small rental) | 10% |

Numeric rebalancing example: if markets push equities from 30% to 36% (portfolio becomes 36/24/30/10), sell 6% of equity gains and move 3% into fixed income and 3% into passive project funding to restore balance.

Tracking Progress and Rebalancing Assets

Review the allocation every six months (or sooner if life changes). Regular rebalancing keeps the risk profile steady and converts gains into stability. Set a recurring calendar reminder and keep a one‑page allocation sheet in your accounts so you can track changes in time and money.

Micro‑action: create a one‑page allocation sheet this week showing current percentages, target percentages and the next review date.

Common Pitfalls and Mistakes to Avoid

Success in building a side income depends as much on what people avoid as what they do. The promise of rapid gains can distract from steady progress. Recognising common traps early makes it easier to build resilient income streams.

❌ Sab kuch ek saath start karna

❌ Skill develop kiye bina income expect karna

❌ Income ko invest na karna

❌ जल्दी passive income expect karna

👉 Reality: Time lagta hai, consistency chahiye

The Danger of Spreading Resources Too Thin

Trying to launch too many projects at once is a frequent mistake. Splitting time, money and attention across several unfinished ideas usually prevents meaningful traction. It is better to focus on one income idea, reach a basic level of product‑market fit, then scale before adding another stream.

Ignoring the Importance of Emergency Funds

Many people begin investing or creating products without first securing a safety net. An emergency fund (3–6 months of essential expenses) protects against unexpected events such as illness or job loss. Without it, people may be forced to sell investments at a loss or abandon promising projects.

Falling for Get‑Rich‑Quick Schemes

The internet is full of offers that promise high returns with little effort. These are often red flags. Typical warning signs include guaranteed high returns, pressure to invest quickly and opaque fee structures. Always verify claims, check regulation and read independent reviews before committing money or time.

Red flags to watch for:

- Unrealistic returns promised in short timeframes.

- High‑pressure sales tactics or urgency to invest immediately.

- Lack of transparent fees, terms or verifiable track record.

| Strategy Element Sustainable Approach Common Mistake | ||

| Focus | Deep work on one project | Multitasking too many ideas |

| Safety | Building an emergency fund | Investing all available cash |

| Growth | Long‑term compounding | Chasing quick‑fix schemes |

| Research | Verifying market demand | Trusting unverified promises |

Example: a generic “get rich fast” trading course that guarantees 20% monthly returns is a typical offer to avoid; legitimate investing carries risk and no guaranteed short‑term returns. If in doubt, consult a certified financial adviser or refer to regulator guidance (for UK readers: FCA; for Indian readers: SEBI) on spotting scams.

Micro‑action: list three potential red flags you might have ignored in the past and commit to one safeguard (e.g. an emergency account or due diligence checklist) before investing further time or money.

Managing Expectations Regarding Time and Effort

Building reliable revenue streams usually takes more time and effort than beginners expect. Many people hope for instant results, but developing meaningful passive income is a gradual process. Think of financial independence as a marathon, not a sprint.

- ⏳ 3–6 months → First side income

- ⏳ 1–2 years → Strong second income

- ⏳ 3–5 years → Financial stability

The Reality of the Initial Labour Phase

The early phase demands concentrated time, energy and effort before income becomes steady. Many passive projects require a focused “build” period that can range widely depending on the model and market — a practical guideline is 12–24 months, but timelines vary.

Consistency matters most in this phase. Whether someone is creating a course, publishing content or building an investment portfolio, the lack of quick returns often leads to frustration. Keeping a steady routine and realistic milestones helps prevent burnout.

Transitioning from Active Effort to Passive Returns

The shift from active work to passive returns happens slowly. At first, time is exchanged directly for money; over time, systems, products and investments begin to yield returns with less daily input. This allows a person to spend more time on scaling rather than constant creation.

Understanding this evolution reduces the risk of quitting too early. Treat each project as a long‑term experiment and measure progress by small wins — traffic, sign‑ups, repeat sales or monthly dividend receipts.

What to expect (rough timeline):

- Months 1–3: Research, validation and early creation — high effort, little income.

- Months 4–12: Launch and optimisation — medium effort, early revenue signals.

- 12+ months: Scaling and maintenance — lower ongoing effort per unit of revenue as systems mature.

| Type, Initial Effort, Time to Maturity, Maintenance Level | |||

| Digital Products (courses, e‑books) | High | 12–18 months | Low |

| Dividend Stocks | Medium | 24+ months | Very Low |

| Rental Property | High | 18–24 months | Medium |

| Content / YouTube channel | Very High | 12–24 months | Medium |

Practical CTA: choose one small project and commit to a 12‑week test. Track weekly hours spent and simple progress metrics (leads, sales, views or dividend receipts) to judge whether to persevere, pivot or stop. This controlled approach helps people learn quickly while protecting time and energy.

Navigating the Taxation Aspect of Diverse Income

Tax planning is a vital part of successful income diversification in India. As people add freelance gigs, investment returns and small businesses, their tax picture becomes more complex. Understanding how different streams are taxed helps protect net returns and avoid surprises.

- Blogging income → Business income

- Freelancing → Professional income

- Capital gains → Separate taxation

- Proper tax planning zaroori

👉 Smart tax planning = higher net income

Understanding Income Tax Slabs in India

India uses a slab‑based income tax system, where higher income is taxed at higher rates. When assessing any income stream, calculate the net return after tax rather than focusing on gross receipts. Note that slab rates and thresholds change regularly — check the latest government guidance before making decisions.

“In this world, nothing can be said to be certain, except death and taxes.”

Tax Implications for Freelance and Business Income

Freelance and small business earnings are treated differently from salaried income. These receipts are usually reported under business or professional income and allow for business expense deductions — for example, software subscriptions, marketing costs or home office expenses. Keeping clear records and separate accounts is essential.

Practical tips:

- Keep a dedicated account for business receipts and expenses.

- Save invoices, bills and receipts to support allowable deductions.

- Consider the presumptive taxation scheme if eligible — it can simplify bookkeeping by allowing a fixed percentage of gross receipts as taxable income.

Utilising Tax‑Efficient Investment Vehicles

Investors often use government‑approved instruments to improve tax efficiency within a diversified portfolio. Common options for Indian residents include the Public Provident Fund (PPF) and Equity Linked Savings Schemes (ELSS), both of which offer tax benefits alongside growth potential.

Before choosing investments, weigh liquidity, tax treatment and time horizon. For those who prefer lower capital or easier entry, REITs and stock funds provide property or equity exposure without direct ownership of rental properties.

Common investment types and typical tax treatment:

| Investment Type, Tax Benefit, Liquidity | ||

| PPF | Tax‑exempt growth (E‑E‑E) | Low |

| ELSS | Section 80C deduction, tax‑efficient equity | Medium |

| Fixed Deposits | Interest taxable | High |

Illustrative example (simplified): a freelancer earning ₹50,000/month who claims ₹10,000 of allowable expenses will be taxed on ₹40,000 of monthly profit (annualised), subject to slab rates and any deductions claimed.

What to do now:

- Register a separate business account and start simple bookkeeping.

- Keep digital copies of receipts and invoices.

- Book a tax review with a qualified chartered accountant to tailor planning (especially if using PPF, ELSS, REITs or stock investments).

Note: tax rules change and can be jurisdiction‑specific; the above is general guidance for India. Readers outside India should consult local rules or a local tax professional before acting.

Golden Rule for Wealth Creation

👉 Earn → Save → Invest → Reinvest → Multiply

Yahi real game hai

Conclusion

True wealth is built by steady progress, not by chasing overnight results. Start from your current position, avoid unnecessary debt and focus on small, consistent actions that grow over time. These simple habits create a more secure long-term financial foundation.

Many people wonder how to balance a main job with a side income. The practical answer is to use limited pockets of time each week for high‑impact tasks: create small products, automate routine work and protect cash in a dedicated account. Over months and years, these small actions compound into meaningful passive income and greater financial choice.

Multiple income streams sirf extra paisa nahi dete —

👉 peace of mind + security + freedom dete hain

Start small

Stay consistent

Focus on skills

👉 Aaj ek stream shuru karo, kal life change hogi

Three immediate next steps:

- Open or tidy one account for emergency savings and aim for 3–6 months of essential expenses.

- List your current income sources and map them to the earned / portfolio / passive framework; pick one small idea to test for 12 weeks.

- Commit to one learning action this week (read a short guide, watch a tutorial or schedule a two‑hour work block) to move that idea forward.

These 2026 finance tips form a practical roadmap for people ready to take control of their money. Wealth building is a long‑term journey: remain patient, keep experiments small and scale the streams that show clear results. For ongoing support, consider subscribing for weekly income ideas, downloadable templates and short checklists to guide each step.

FAQ

What is the fundamental difference between active and passive income?

Bottom line: active income is time traded for money; passive income is front‑loaded effort or capital that later yields ongoing returns. Active examples include a monthly salary or freelance hourly work. Passive examples include a digital course, rental income from property or dividends from stocks — these typically need more initial effort or investment but less daily time once established.

Why is income diversification considered a priority in 2026 finance tips?

Bottom line: diversification reduces the risk of a single point of failure. If one income stream falls, other streams (salary, investments, digital products) can keep money coming in. This is especially important in volatile markets and for people who want financial breathing room during career changes.

How much should someone save before starting a side income venture?

Bottom line: aim for an emergency account covering 3–6 months of essential expenses, adjusted for personal circumstances. That buffer lets people test income ideas — a small digital product, freelance work or a blog — without risking core living costs.

Which platforms are best for building multiple income streams in the Indian market?

Bottom line: use platforms that match the chosen stream. For freelance work, Upwork and Fiverr connect to global clients. For investments, regulated brokers and apps such as Zerodha or Groww (or local equivalents) support SIPs into mutual funds and equities. For digital products, consider Udemy, Teachable, YouTube or a self‑hosted site. Choose one channel and test it for a few months before expanding.

What is a realistic timeline to see results from passive income?

Bottom line: expect 12–24 months for many passive projects to mature, though this varies by model. Example: a simple online course might take 6–12 months to build and another 6–12 months to reach steady sales; a rental property may take longer to cover costs and show net rental income. Track time invested and key metrics to judge progress.

How are diverse income streams taxed for Indian residents?

Bottom line: different streams have different tax rules. Freelance income is often filed under ‘Profits and Gains of Business or Profession’ and may allow expense deductions. Investments have varied treatment (dividends, capital gains, PPF/ELSS benefits). Keep separate accounts for business receipts and expenses and consult a tax professional for personalised advice.

What are common ideas and opportunities to consider for building income streams?

Bottom line: match ideas to time, capital and skills. Popular options include freelancing, digital products (courses, e‑books), content channels (YouTube, blogs), systematic investments (SIPs in mutual funds, stocks) and property or REITs for rental income. Affiliate marketing, stock photos and niche digital products are other low‑capital options to explore.

How long should I test an income idea before deciding to stop?

Bottom line: use a time‑boxed experiment — 12 weeks is a practical minimum. Track simple metrics (leads, sales, views, hours spent, and money earned). If there is measurable progress after 12 weeks, continue; if not, review assumptions or pivot to a new idea.

How can I protect myself from risky platforms or scams?

Bottom line: watch for red flags — guaranteed returns, pressure to act fast, unclear fees or unverifiable track records. Verify platform credentials, read independent reviews, keep records and consult regulator guidance (SEBI in India, FCA in the UK) or a certified adviser if unsure.

Where can I get more help and practical tools?

Bottom line: start with simple templates and short guides. Download a 12‑week action plan or an allocation sheet to track accounts and time. Subscribe for weekly income ideas, step‑by‑step checklists and short tutorials to guide the next steps.

Is blogging still profitable in 2026?

Yes, agar SEO + consistency follow karein to blogging still highly profitable hai.

How many income streams should I have?

At least 2–3 income streams for financial safety.

Best passive income ideas in India?

Mutual funds, dividend stocks, blogging, rental income.

Can I start with low investment?

Yes, blogging & freelancing zero investment se start ho sakta hai.

Disclaimer

This publication is intended solely for informational and educational purposes and does not constitute professional, legal, tax, or financial advice. The information provided has been compiled from sources believed to be reliable; however, its accuracy, completeness, or current relevance is not guaranteed. The views and opinions expressed herein reflect the author’s understanding at the time of publication and are subject to change without notice. Readers are strongly advised to seek independent professional advice before making any decision or taking any action based on the information contained in this publication. The author and publisher expressly disclaim any responsibility or liability for any loss, damage, or consequence arising directly or indirectly from reliance on this content or from any action taken or not taken based on it.