Transitioning away from a monthly salary marks a significant life shift. Many individuals find that without careful retirement planning, their hard-earned savings can diminish faster than expected.

The economic landscape in 2026 presents unique hurdles that require a proactive approach. It is essential to organise your finances effectively to maintain a comfortable lifestyle while navigating global uncertainties.

Retirement ke baad sabse bada sawaal hota hai —

👉 “Ab regular income kaise aayegi?”

Jab salary band ho jaati hai, tab planning galat ho to savings dheere-dheere khatam hone lagti hai.

Isliye 2026 mein retirement ke baad sirf paisa banana nahi, balki paisa sambhalna aur use wisely use karna sabse important hai.

Is blog mein hum simple language mein samjhenge:

✔ Safe income kaise generate karein

✔ Kaun se investment best hain

✔ Kaun si galtiyaan avoid karni chahiye

By adopting a robust strategy, you can ensure long-term stability. This guide explores how to secure your future, allowing you to enjoy your golden years with confidence and financial peace.

Key Takeaways

- Prioritise the organisation of your pension assets early.

- Emphasise the need for a diversified investment portfolio.

- Regularly monitor your expenditure to avoid unnecessary losses.

- Seek professional advice to customise your financial path.

- Focus on capital preservation to ensure lasting stability.

Understanding the Financial Landscape for Retirees in 2026

The financial landscape for retirees in 2026 is shifting due to new tax laws and interest rate fluctuations. Effective financial planning 2026 requires a keen awareness of these structural changes to ensure your corpus remains resilient. Retirees must now navigate a complex environment where traditional income sources may not perform as they once did.

Retirement ke baad 4 bade risks hote hain:

1. Inflation Risk

Aaj ₹50,000 ka expense hai, 10–15 saal baad ₹1 lakh bhi ho sakta hai.

2. Medical Expenses

Age ke saath health cost badhti hai.

3. Longevity Risk

Log ab 80–85 saal tak jee rahe hain → paisa zyada time tak chalana padega.

4. Market Risk

Agar saara paisa market mein daal diya aur crash aa gaya → problem ho sakti hai.

The Impact of Inflation on Fixed Incomes

Inflation acts as a silent thief, gradually eroding the purchasing power of your monthly pension or interest payouts. In 2026, even moderate price increases can significantly reduce the standard of living for those relying on static income streams. It is essential to recognise that money which covers your needs today may fall short in the coming years.

To combat this, retirees should integrate inflation-adjusted assets into their broader financial planning 2026 strategy. Relying solely on fixed-interest instruments often leaves a portfolio vulnerable to the rising cost of essential goods. Diversification remains the most reliable defence against the long-term effects of rising prices.

Changing Healthcare Costs and Insurance Needs

Healthcare expenses represent one of the most significant variables in retirement budgeting. As medical technology advances and service costs climb, the financial burden on seniors continues to grow. Comprehensive health insurance is no longer just an option; it is a fundamental pillar of security for every retiree.

Many individuals find that their existing coverage is insufficient for the realities of 2026. Proactive financial planning 2026 involves reviewing your insurance policies to ensure they cover modern treatments and potential long-term care. Taking these steps early provides peace of mind and protects your savings from being depleted by unexpected medical emergencies.

How to Manage Money After Retirement in 2026 (Safe Income Strategy for Peaceful Living)

Building a reliable retirement income strategy is the cornerstone of a stress-free life after your professional career ends. As you enter this new chapter in 2026, the focus must shift from aggressive wealth accumulation to the careful preservation and distribution of your assets. A thoughtful approach ensures that your hard-earned savings provide a steady stream of funds while remaining resilient against market volatility.

Agar aap retirement ke liye corpus banana chahte hain, to yeh detailed guide zaroor padhein”

➡ Link: Retirement Corpus Blog Retirement Corpus Needed in India: A 2026 Guide

Prioritising Liquidity and Safety

The first step in your financial journey is ensuring that your immediate needs are met without disrupting your long-term investments. You should maintain a portion of your corpus in highly liquid assets to handle unexpected expenses or medical emergencies. Liquidity provides the peace of mind that you can access cash instantly when life throws a curveball.

To achieve this, consider these essential steps for maintaining a secure financial base:

- Keep at least 12 to 24 months of living expenses in a high-yield savings account or liquid mutual fund.

- Explore safe investment options that offer capital protection, such as government-backed schemes.

- Ensure that your emergency fund is separate from your primary investment portfolio to avoid premature withdrawals.

Balancing Growth with Capital Preservation

While safety is paramount, you cannot ignore the silent threat of inflation. If your money does not grow at a rate that outpaces rising costs, your purchasing power will decline over time. Therefore, you must strike a delicate balance between preserving your capital and seeking modest growth.

A resilient portfolio often combines fixed-income instruments with a small, strategic allocation to equities. This blend allows your retirement income to keep pace with the economy while protecting the bulk of your corpus from significant market downturns. By choosing safe investment options that offer a mix of stability and growth, you create a sustainable structure that supports your lifestyle for decades to come.

Mastering the Safe Withdrawal Strategy

Establishing a sustainable withdrawal plan is the cornerstone of a peaceful retirement. Many individuals find that the transition from accumulating wealth to spending it requires a significant shift in mindset. By implementing a Safe Withdrawal Strategy, retirees can enjoy their hard-earned savings without the constant fear of running out of money prematurely.

Retirement ke baad sabse important rule hai:

👉 “3–4% Withdrawal Rule”

Iska matlab:

Aap apne total corpus ka sirf 3–4% har saal nikaalein.

Example:

Agar aapke paas ₹1 crore hai:

- 4% = ₹4 lakh per year

- Matlab ≈ ₹33,000 per month

👉 Isse aapka paisa long-term tak safe rehta hai.

The Golden Rule of Retirement Withdrawals

The primary objective of any withdrawal plan is to ensure that your corpus lasts for your entire lifetime. A common guideline suggests limiting annual distributions to a percentage that allows the remaining balance to continue growing. Consistency is key, but you must also remain mindful of statutory requirements.

In India, while specific tax laws apply, it is important to remember that Required Minimum Distributions (RMDs) are a global standard in many retirement systems. Currently, these mandatory withdrawals typically begin once you turn 73, with the age threshold set to rise to 75 starting in 2033. Planning your Retirement Withdrawals around these dates helps you maintain compliance while managing your tax liabilities effectively.

Adjusting Withdrawal Rates Based on Market Conditions

Market volatility can significantly impact the longevity of your portfolio. If you withdraw a fixed amount during a market downturn, you risk selling assets at depressed prices, which is known as the sequence of return risk. To mitigate this, you should adopt a flexible approach to your annual spending.

When markets perform well, you might consider taking a slightly higher distribution to cover extra expenses or travel. Conversely, during periods of economic instability, it is wise to tighten your budget and reduce your withdrawal rate. This dynamic adjustment ensures that your capital remains preserved for future needs, providing you with greater peace of mind throughout your retirement years.

Designing an Ideal Asset Allocation Model

Achieving financial peace of mind requires a carefully designed asset allocation model. By spreading investments across different categories, a retiree can protect their capital while ensuring steady growth. This strategy helps manage the inherent risks of the market while meeting personal financial goals.

Retirement ke baad risk kam aur stability zyada honi chahiye.

Asset allocation blog link Where Should You Invest ₹10 Lakhs in 2026? Smart Asset Allocation Strategy for Stable & Growing Income

Suggested Allocation:

- 🟢 50–60% → Safe Instruments (FD, SCSS, Bonds)

- 🔵 20–30% → Mutual Funds (SWP option)

- 🟡 10–15% → Equity (growth ke liye)

- 🟠 5–10% → Gold (safety hedge)

👉 Yeh mix aapko income + growth + safety deta hai.

The Role of Debt Instruments in a Portfolio

Debt instruments act as the anchor for any retirement portfolio. They provide the stability needed to cover essential monthly expenses without the worry of market volatility. In the Indian context, these often include government-backed schemes, fixed deposits, and high-quality corporate bonds.

These assets offer predictable returns, which are vital for maintaining a consistent cash flow. By prioritising safety, retirees can ensure that their basic needs are met regardless of how the stock market performs. This conservative approach forms the bedrock of a secure financial future.

Incorporating Equity for Long-Term Growth

While safety is paramount, ignoring growth can be a mistake due to the rising cost of living. Incorporating equity into a portfolio allows the corpus to grow over time, effectively acting as a hedge against inflation. Even a modest exposure to equity mutual funds can significantly boost the longevity of retirement savings.

Determining the Equity-to-Debt Ratio

Finding the right balance between risk and reward is a personal journey. The ideal equity-to-debt ratio depends on an individual’s health, existing pension income, and overall risk appetite. A common rule of thumb suggests that as one ages, the allocation to debt should gradually increase to preserve capital.

The following table illustrates how different risk profiles might structure their investments to achieve a balanced outcome:

| Risk Profile | Equity Allocation | Debt Allocation | Primary Goal |

|---|---|---|---|

| Conservative | 20% | 80% | Capital Preservation |

| Moderate | 40% | 60% | Balanced Growth |

| Aggressive | 60% | 40% | Wealth Appreciation |

Ultimately, the goal is to create a structure that supports both immediate income needs and future security. Regular reviews ensure that the portfolio remains aligned with changing life circumstances and market conditions.

Top Investment Options for Indian Retirees in 2026

Building a reliable stream of retirement income in 2026 involves a mix of government-backed schemes and market-linked products. Choosing the right senior citizen investment strategy is essential to ensure your capital lasts throughout your golden years. By diversifying across different asset classes, you can create a portfolio that balances safety with consistent returns.

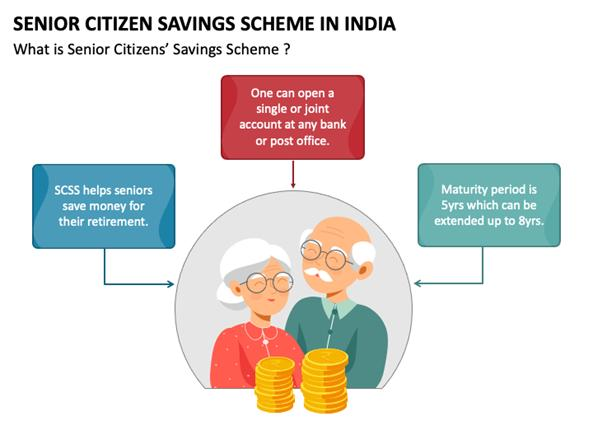

Senior Citizen Savings Scheme (SCSS) Benefits

The Senior Citizen Savings Scheme (SCSS) remains a cornerstone for many retirees in India. It is widely considered one of the safest investment options due to its government backing and attractive interest rates. Investors benefit from quarterly interest payouts, which provide a predictable cash flow for daily expenses.

The scheme is specifically designed for individuals aged 60 or over, offering a secure way to park retirement funds. Because the interest is paid regularly, it helps in maintaining liquidity without exposing the principal amount to market volatility. SCSS is an excellent choice for those who prioritise capital protection above all else.

👉 Interest Rate: ~8.2% p.a. (quarterly payout)

👉 Maximum Limit: ₹30 lakh (2026 approx)

👉 Lock-in: 5 years (extendable)

📝 Kaise Invest Karein?

- Post Office ya authorized bank mein account kholein

- Form + PAN + Aadhaar + age proof

- Lump sum deposit

👉 Government-backed safest option

👉 Regular quarterly income

💰 Example:

- Investment: ₹30 lakh

- Interest rate: ~8.2% (approx)

- Annual income: ₹2.46 lakh

- Monthly equivalent: ~₹20,500

✔ Safe + predictable income

✔ Ideal for basic expenses

Systematic Withdrawal Plans (SWP) from Mutual Funds

For those seeking passive income after retirement that can potentially beat inflation, a SWP from mutual funds is a powerful tool. This method allows you to withdraw a fixed amount from your investment at regular intervals. It provides flexibility, as you can adjust the withdrawal amount based on your changing financial needs.

By opting for an SWP, you keep your remaining corpus invested in the market. This allows your money to grow over time, which is a significant advantage compared to traditional savings accounts. It is a smart way to manage your cash flow while keeping your long-term financial goals on track.

👉 Expected Return: ~10–12% (long term, not fixed)

👉 Limit: No limit

👉 Lock-in: Scheme par depend karta hai

📝 Kaise Invest Karein?

- AMC website / app / advisor ke through

- Lump sum invest karke SWP set karein (monthly withdrawal)

👉 Smart & tax-efficient income option

👉 Capital growth + withdrawal dono possible

💰 Example:

- Investment: ₹20 lakh

- Expected return: ~10–12% (long term)

- Monthly withdrawal: ₹12,000 – ₹15,000 possible

✔ Tax efficient

✔ Inflation beating potential

⚠️ Market risk thoda hota hai → isliye limited allocation rakhein

Pradhan Mantri Vaya Vandana Yojana and Annuity Plans

Government-backed initiatives like the Pradhan Mantri Vaya Vandana Yojana (PMVVY) offer guaranteed pension returns for senior citizens. These plans provide a fixed income for a specific period, ensuring that you are not affected by fluctuating interest rates in the broader economy. They serve as a reliable foundation for your monthly budget.

Annuity plans from insurance companies also offer a similar structure, providing a lifelong income stream. While these plans may offer lower growth potential, they provide peace of mind through guaranteed payouts. Combining these with other instruments creates a robust safety net for your future.

👉 Interest/Pension Rate: ~7.4% p.a.

👉 Maximum Limit: ₹15 lakh per person

👉 Tenure: 10 years

📝 Kaise Invest Karein?

- LIC office ya online LIC portal

- Monthly/quarterly pension option choose karein

👉 Pension-type scheme (LIC backed)

👉 Fixed monthly/quarterly income

💰 Example:

- Investment: ₹15 lakh

- Return: ~7.4%

- Annual income: ₹1.11 lakh

- Monthly income: ~₹9,250

✔ Stable pension flow

✔ Useful for fixed monthly expenses

RBI Floating Rate Bonds

👉 Government bonds

👉 Interest linked with NSC rate (changes periodically)

💰 Example:

- Investment: ₹20 lakh

- Return: ~7.5%

- Annual income: ₹1.5 lakh

- Monthly equivalent: ~₹12,500

✔ Safe + slightly flexible return

✔ Good for diversification

👉 Interest Rate: ~7.5% (NSC + spread, changes periodically)

👉 Maximum Limit: No upper limit

👉 Lock-in: 7 years

📝 Kaise Invest Karein?

- Selected banks (SBI, HDFC, etc.)

- Online ya branch se apply karein

✔ Best for: Safe + slightly flexible returns

Bank Fixed Deposits (FDs)

FD aur Debt Mutual Fund ke beech difference samajhne ke liye yeh comparison zaroor dekhein”

➡ Link: FD vs Debt Mutual Fund Blog Invest Wisely in 2026: Fixed Deposits vs Mutual Funds vs Bonds vs Gold

👉 Most popular option

👉 Easy liquidity

💰 Example:

- Investment: ₹15 lakh

- Interest: ~7%

- Annual income: ₹1.05 lakh

- Monthly equivalent: ~₹8,750

⚠️ Limitation:

- Inflation ko beat nahi karta

✔ Use for short-term stability

👉 Interest Rate: ~6.5% – 7.5% (senior citizens ko extra milta hai)

👉 Maximum Limit: No limit

👉 Tenure: Flexible (7 days to 10 years)

📝 Kaise Invest Karein?

- Kisi bhi bank mein online/offline FD bana sakte hain

✔ Best for: Liquidity + short-term safety

⚠️ Note: Inflation ko beat nahi karta

📊 Comparison Table :-

👉 Is table ko blog ke beech mein insert karein (reader ko quick clarity milegi)

| Investment Option | Interest Rate | Max Limit | Lock-in | Risk Level | Best For |

|---|---|---|---|---|---|

| SCSS | ~8.2% | ₹30 lakh | 5 years | Very Low | Fixed income |

| PMVVY | ~7.4% | ₹15 lakh | 10 years | Very Low | Pension income |

| RBI Bonds | ~7.5% | No limit | 7 years | Very Low | Safe returns |

| Bank FD | ~6.5–7.5% | No limit | Flexible | Low | Liquidity |

| MF (SWP) | ~10–12%* | No limit | Depends | Moderate | Growth + income |

*Not fixed (market-linked)

Practical Monthly Income Planning Example

A well-structured budget transforms the way retirees view their monthly cash flow. By mapping out every rupee, individuals can enjoy their golden years without the constant worry of running out of funds. Establishing a reliable stream of passive income after retirement is the first step toward this financial freedom.

Complete Retirement Income Example (₹1 Crore Plan)

Possible Allocation:

- ₹40 lakh → SCSS + FD

- ₹30 lakh → SWP (Mutual Funds)

- ₹20 lakh → Bonds

- ₹10 lakh → Equity/Gold

👉 Isse approx ₹50,000 – ₹70,000 monthly income generate ho sakti hai (combined strategy se

| Investment Option | Amount | Monthly Income |

|---|---|---|

| SCSS | ₹30 lakh | ₹20,500 |

| PMVVY | ₹15 lakh | ₹9,250 |

| RBI Bonds | ₹20 lakh | ₹12,500 |

| FD | ₹15 lakh | ₹8,750 |

| SWP (MF) | ₹20 lakh | ₹12,000–15,000 |

Creating a Cash Flow Budget

To begin, one must list all sources of monthly inflows. This includes pension payments, interest from fixed deposits, and dividends from mutual funds. Clarity is essential when tracking these figures to ensure the total matches the expected lifestyle needs.

Next, list all recurring monthly expenses. This list should cover everything from utility bills and groceries to medical insurance premiums. Subtracting these costs from the total income reveals the surplus available for other activities.

Aap yeh bhi samajh sakte hain ki retirement se pehle kitna monthly invest karna zaroori hai”

➡ Link: Monthly Investment Blog How Much Should You Invest Every Month in 2026?

Allocating Funds for Essential and Discretionary Expenses

Effective money management relies on smart fund allocation. Retirees should prioritise essential costs first to ensure that basic needs are always met. Once these are covered, the remaining balance can be directed toward discretionary spending.

Consider the following breakdown for a balanced monthly plan:

- Essential Expenses: Rent, electricity, groceries, and healthcare.

- Discretionary Spending: Travel, hobbies, and social outings.

- Emergency Buffer: A small portion set aside for unexpected repairs or medical needs.

By categorising spending, retirees can maintain a sustainable passive income after retirement. This disciplined approach prevents the erosion of the core capital corpus. Ultimately, consistent monitoring of these categories allows for a comfortable and dignified lifestyle throughout the retirement years.

Emergency fund retirement planning ka sabse important pillar hai — is guide ko zaroor padhein”

➡ Link: Emergency Fund Blog Where to Stash Your Emergency Fund in 2026

Navigating Tax Efficiency in Retirement

Smart tax planning acts as a silent partner in your retirement journey, helping you retain more of your hard-earned money. By understanding the rules, you can ensure that your income remains stable while minimising unnecessary outflows to the tax authorities. Adopting a proactive tax efficiency strategy is essential for long-term financial health.

Optimising Tax on Interest Income

Interest earned from fixed deposits and savings accounts often forms the backbone of a retiree’s income. However, this income is typically taxable at your applicable slab rate. To manage this, you should be aware of the specific benefits available to senior citizens.

Tax Benefits to Senior Citizens under Income Tax Act 2025 (Brief with Sections)

Income Tax Act 2025 ne largely existing benefits ko continue rakha hai, with some simplification. Senior citizens (60+) ko extra relief + compliance ease diya gaya hai.

🟢 1. Higher Basic Exemption Limit (Old Regime)

👉 Senior Citizen (60–80 years): ₹3 lakh

👉 Super Senior Citizen (80+): ₹5 lakh

✔ Matlab: Is limit tak income par koi tax nahi

“Old vs New tax regime ka comparison samajhne ke liye yeh article aapke liye useful hoga”

➡ Link: Income Tax Slab BlogIncome Tax Slabs 2026: Old vs New Regime – Smart Tax Tips

🔵 2. Section 80TTB – Interest Income Deduction ( Section 153 IT ACT 2025)

👉 Deduction up to ₹50,000 on:

- Bank FD interest

- Savings account interest

- Post office deposits

✔ Special benefit for retirees (interest income main source hota hai)

🟡 3. Section 80D – Health Insurance / Medical Expense (Section 126under IT Act2025)

👉 Deduction up to ₹50,000

✔ Even medical expenditure allowed if no insurance

✔ Very useful for senior citizens

🟠 4. Section 80DDB – Critical Illness Treatment ( Section 128 under IT Act 2025)

👉 Deduction up to ₹1,00,000 (senior citizens)

✔ For diseases like cancer, kidney failure, etc.

🔴 5. Section 80C – Investment Deduction (Section 123 under IT Act 2025)

👉 Deduction up to ₹1.5 lakh

✔ Options include:

- LIC premium

- PPF

- 5-year FD

🟣 6. Standard Deduction (Section 16 – Pensioners)

👉 ₹50,000 (Old Regime)

👉 ₹75,000 (New Regime approx)

✔ Pension = salary treated → deduction allowed

🟤 7. Section 194P – No ITR Filing (Very Important)( Section 393(1) table under IT Act 2025

👉 Applicable for 75+ senior citizens

Conditions:

- Only pension + interest income

- Same bank

✔ Bank TDS deduct karega → ITR file karne ki zaroorat nahi

⚫ 8. Higher TDS Threshold on Interest

👉 Up to ₹1 lakh interest par TDS nahi (approx new provisions)

✔ Cash flow better hota hai

⚪ 9. Section 87A – Rebate Benefit ( Section 156 of IT Act 2025)

👉 Income certain limit tak ho to tax zero

✔ Old regime: up to ₹5 lakh

✔ New regime: higher limit (approx ₹12 lakh range)

Utilising Tax-Efficient Withdrawal Methods

How you withdraw your funds can be just as important as how you invest them. Instead of pulling money from high-tax accounts first, consider a sequence that prioritises tax-deferred or tax-exempt sources. This strategic approach helps keep your annual taxable income in lower brackets.

Systematic Withdrawal Plans (SWP) from mutual funds are often more tax-efficient than traditional interest-bearing instruments. Because you are only taxed on the capital gains portion of your withdrawal, your overall tax burden is often reduced. Diversifying your withdrawal sources is a powerful way to protect your corpus from tax erosion over time.

Ultimately, staying informed about current regulations allows you to make better decisions. By balancing your income streams and utilising available deductions, you can enjoy a more peaceful and secure retirement. Remember that small adjustments to your withdrawal timing can lead to substantial savings over the years.

Common Financial Mistakes to Avoid

Financial security in your golden years depends as much on what you avoid as what you invest in. Many individuals find that Retirement Mein Common Mistakes (Avoid Karein) is a vital mantra for maintaining a stable lifestyle. By identifying these traps early, you can protect your corpus from unnecessary erosion.

❌ 1. Saara paisa FD mein daal dena

👉 Inflation se value girti rahegi

❌ 2. High-risk investment karna

👉 Loss ka risk zyada

❌ 3. Emergency fund na rakhna

👉 Medical emergency mein problem

❌ 4. Tax planning ignore karna

👉 Net income kam ho jayegi

Over-relying on Traditional Savings Accounts

It is common for retirees to keep the bulk of their funds in standard savings accounts for the sake of liquidity. However, these accounts often offer interest rates that fail to keep pace with the rising cost of living. Inflation acts as a silent thief, gradually reducing the purchasing power of your money over time.

Instead of keeping all your cash in a low-yield account, consider diversifying into higher-yielding instruments. While safety is paramount, a balanced approach ensures your money grows enough to sustain your lifestyle for decades.

Ignoring the Impact of Rising Healthcare Costs

Medical inflation in India is significantly higher than general inflation. Many retirees fail to account for the steep rise in hospitalisation expenses as they age. Relying solely on personal savings to cover these costs can quickly deplete your retirement fund.

It is essential to maintain a dedicated health insurance policy or a separate medical emergency fund. Ignoring this reality is one of the most significant Retirement Mein Common Mistakes (Avoid Karein) that can lead to severe financial distress during a health crisis.

Falling for High-Risk Investment Scams

Retirees are often targeted by fraudulent schemes promising unrealistic, guaranteed returns. These scams frequently disguise themselves as low-risk opportunities to lure those seeking extra income. Always verify the credentials of any investment platform with the SEBI or RBI before committing your capital.

If an offer sounds too good to be true, it almost certainly is. Protecting your assets requires a healthy dose of scepticism and a commitment to due diligence before making any financial decisions.

| Mistake Type | Potential Impact | Recommended Action |

|---|---|---|

| Excessive Savings Cash | Loss of purchasing power | Diversify into debt funds |

| Ignoring Health Costs | Corpus depletion | Buy comprehensive insurance |

| High-Risk Scams | Total loss of capital | Verify with regulators |

Protecting Your Corpus Against Inflation and Healthcare Costs

As you navigate your golden years, safeguarding your retirement corpus against the dual threats of inflation and rising healthcare costs becomes a top priority. While your investments aim to grow, the purchasing power of your money can diminish if you do not plan for these inevitable challenges. Taking a proactive stance ensures that your nest egg remains resilient throughout your retirement journey.

Inflation ka impact samajhna bahut zaroori hai — yeh dheere-dheere aapki savings ki value kam karta hai”

➡ Link: Inflation Blog Inflation Quietly Destroys Your Wealth (2026 Guide)

The Importance of Comprehensive Health Insurance

Medical expenses often represent the highest variable cost for retirees. Relying solely on personal savings to cover major surgeries or chronic conditions can quickly deplete your wealth. Comprehensive health insurance acts as a vital shield, preventing these high costs from eating into your long-term financial plans.

It is wise to choose a policy that offers adequate coverage for both hospitalisation and outpatient care. By transferring the risk of expensive medical treatments to an insurer, you protect your capital for its intended purpose: funding your lifestyle. Always review your policy annually to ensure it keeps pace with medical inflation.

Maintaining an Emergency Fund for Unforeseen Events

Life in retirement can be unpredictable, and having a dedicated emergency fund is essential for peace of mind. This pool of liquid cash allows you to handle sudden expenses without the need to sell your long-term investments during a market downturn. It serves as a buffer that keeps your financial strategy intact.

Consider the scale of potential needs when setting your target amount. For instance, in some regions, assisted living facilities can reach an annual median cost of $70,800, highlighting why liquidity is so critical. By keeping a portion of your assets in high-yield savings or liquid funds, you ensure that you are prepared for any unforeseen events that may arise.

The Way Forward for Long-Term Financial Security

The journey toward long-term financial security does not end the moment you retire. While initial retirement planning provides a solid foundation, the real work involves staying vigilant as your needs and the market environment shift over time. By remaining proactive, you ensure that your hard-earned savings continue to support your lifestyle for years to come.

Regular Portfolio Reviews and Rebalancing

Markets are rarely static, and your investment portfolio should reflect that reality. Conducting a thorough review at least once a year helps you determine if your current asset allocation still aligns with your risk tolerance and income requirements. If certain assets have performed exceptionally well, they might now represent a larger portion of your portfolio than intended.

Rebalancing is the essential process of selling some of your high-performing assets and reinvesting in underweighted areas to restore your original balance. This disciplined approach prevents you from taking on unintended risks while keeping your retirement planning strategy on track. It is a simple yet powerful way to lock in gains and maintain a steady course toward your financial goals.

Planning for Estate and Legacy Distribution

True peace of mind comes from knowing that your affairs are in order and your loved ones are protected. Effective estate planning ensures that your assets are distributed exactly as you wish after you are gone. This process involves more than just writing a will; it requires a clear understanding of your legal and financial obligations.

Consider consulting with a legal professional to draft a comprehensive estate plan that covers your bank accounts, property, and investment holdings. By clearly documenting your intentions, you reduce the burden on your family during difficult times. Integrating this step into your broader retirement planning provides the ultimate assurance that your legacy remains secure and your family is well-provided for in the future.

Conclusion

Achieving a peaceful retirement requires a shift in how one views personal wealth. Moving from a phase of accumulation to one of distribution demands a disciplined mindset. Effective financial planning 2026 provides the structure needed to protect your hard-earned savings against rising costs.

Retirees often find that success lies in the details of their daily habits. By prioritising liquidity and maintaining a clear view of tax obligations, individuals can enjoy their time without unnecessary stress. This proactive approach ensures that your portfolio remains resilient against market volatility.

Commitment to regular reviews keeps your strategy aligned with your personal goals. Sound financial planning 2026 is your roadmap to legacy and long-term security. Start organising your assets today to build a foundation of stability. A well-managed plan lets you focus on what truly matters in your retirement years.

Retirement ke baad financial success ka secret hai:

✔ Safe income planning

✔ Right asset allocation

✔ Controlled withdrawal

✔ Smart tax strategy

Agar aap passive income create karna chahte hain, to yeh detailed guide bhi zaroor padhein”

➡ Link: Passive Income Blog How to Generate Passive Income in 2026

👉 Yaad rakhiye:

“Retirement mein goal paisa banana nahi, paisa bachana aur sustain karna hai.”

Agar aap sahi planning karte hain, to retirement life stress-free aur financially secure ho sakti hai.

FAQ

Why is financial planning 2026 so critical for those entering retirement today?

The economic landscape has shifted, and financial planning 2026 focuses heavily on the reality that inflation can quickly erode the purchasing power of a fixed income. For effective retirement planning, retirees should look beyond traditional savings and organise their portfolios to handle rising healthcare costs and volatile market conditions, ensuring their retirement income remains sustainable for decades.

What are the most reliable safe investment options for Indian retirees?

To ensure capital preservation, the Senior Citizen Savings Scheme (SCSS) is highly recommended due to its government-backed security and competitive interest rates. Another excellent senior citizen investment is the Pradhan Mantri Vaya Vandana Yojana, offered through the Life Insurance Corporation of India (LIC), which provides a guaranteed payout, making it a cornerstone for those seeking safe investment options.

How can a Systematic Withdrawal Plan (SWP) help in generating passive income after retirement?

An SWP allows an individual to withdraw a specific amount from their mutual fund investments, such as those managed by SBI Mutual Fund or HDFC Mutual Fund, at regular intervals. This strategy is particularly effective for creating passive income after retirement because it is more tax-efficient than standard interest income, as only the capital gains portion of the withdrawal is subject to tax.

What is the “Golden Rule” of retirement withdrawals?

The golden rule suggests that a retiree should aim to withdraw approximately 4% of their total corpus in the first year, adjusting the amount for inflation in subsequent years. By following this strategy, they can maximise the longevity of their savings and mitigate the risk of running out of money, even during periods of poor market performance.

How can retirees reduce their tax liability on their monthly income?

Retirees can optimise their tax efficiency by prioritising tax-saving instruments and using SWP methods, which attract lower tax rates compared to fixed deposits. Additionally, staying informed about the latest deductions available for senior citizens under the Income Tax Act helps in keeping a larger portion of their hard-earned retirement income for personal use.

Why is it a mistake to rely solely on traditional savings accounts?

While traditional savings accounts offer high liquidity, the interest rates often fail to keep pace with inflation. Over-relying on these accounts can lead to a “silent” depletion of wealth. Instead, a balanced approach that includes debt instruments and a small equity exposure is necessary to ensure the portfolio grows enough to cover future expenses.

What role does an emergency fund play in a 2026 retirement strategy?

An emergency fund acts as a vital buffer against unforeseen events, such as urgent home repairs or medical emergencies not fully covered by health insurance from providers like Star Health. By maintaining a liquid fund equivalent to one or two years of expenses, retirees can avoid the need to liquidate their long-term senior citizen investment holdings during a market downturn.

How often should a retirement portfolio be reviewed?

Financial experts recommend that retirees rebalance and review their portfolios at least once a year. This ensures that the asset allocation remains aligned with their risk tolerance and that they are successfully generating the required passive income after retirement despite any shifts in the broader economy or changes in personal health needs.

Disclaimer

This publication is intended solely for informational and educational purposes and does not constitute professional, legal, tax, or financial advice. The information provided has been compiled from sources believed to be reliable; however, its accuracy, completeness, or current relevance is not guaranteed. The views and opinions expressed herein reflect the author’s understanding at the time of publication and are subject to change without notice.

Readers are strongly advised to seek independent professional advice before making any decision or taking any action based on the information contained in this publication. The author and publisher expressly disclaim any responsibility or liability for any loss, damage, or consequence arising directly or indirectly from reliance on this content or from any action taken or not taken based on it.